The Lack of Housing is a Generational Crisis

I've been baffled by the housing market in the United States for my entire adult life. It’s a lesson in unintended policy consequences like no other. While much of the media attention goes to fluctuations in prices and rising mortgage rates, the deeper issues are those of supply and demand.

On the demand side we have Millennial home buyers—the largest birth cohort in US history—emerging onto the housing market seeking to buy homes, followed quickly by Gen Z (the oldest members of Gen Z were born in 1997 and are now in their mid 20s).

Constricting supply, we have a lack of construction of new residential housing, in particular in urban areas where job growth is highest. From the year 2000 until 2021, we went from 120 million housing units to 143 million nationwide, an increase of eighteen percent. But the total nationwide increase isn’t aligned with local demand. Here's Ann Lowrey in The Atlantic on the "underbuilding gap."

The National Association of Realtors compared the issuance of housing permits with the number of jobs created in 174 different metro areas. It found that only 38 metro regions are permitting enough new homes to keep up with job growth; in more than a dozen areas, including New York, the Bay Area, Boston, Los Angeles, Honolulu, Miami, and Chicago, just one new home is getting built for every 20-plus jobs created. The NAR estimates an “underbuilding gap” of as many as 7 million units.

So yes, even though we are building more housing, we’re not building nearly enough where the demand is highest, further driving up costs. Supply is further constrained because the Silent Generation and the Baby Boomers are living longer lives—Bismillah on that one—I am stoked to have the elders with us. However, further constricting supply is just plain bad local policy: insanely difficult permitting processes, overuse of single family zoning, NIMBY-ism (masquerading as historic preservation), and good old-fashioned racism (masquerading as "concerns about preserving neighborhood character").

Median mortgages and median rents in many housing markets nearly outpace the median monthly income. The old guidance used to be that no one should spend more than 30% of their income on rent or mortgage, anything beyond that was considered to be "rent burdened." But according to Pew in 2020 "46% of American renters spent 30% or more of their income on housing, including 23% who spent at least 50% of their income this way." Sometimes you can run by a stat and not really process it but I think it's important to pause on this one: nearly one quarter of American renters are spending 50% of their income on housing with no relief in sight.

Nowhere is this mess more apparent than in the Bay Area but the problem is likely coming soon to a metro near you. The classical definition of inflation is “too much money chasing too little supply.” This is the situation that has unfolded in the Bay. There’s ample demand because of new arrivals and job growth but because of the factors above, there isn’t enough housing being built, leading to soaring costs. The average new mortgage in San Jose is now a staggering $11,000 per month. This week I read a piece in the San Jose Mercury News that I think is worth quoting a length:

While some people choose to rent—and forgo building home equity—because they don’t plan to stay long-term, others can’t afford a down payment or qualify for a mortgage, a “situation that has become increasingly common due to rising mortgage rates and elevated home prices,” Redfin economist Taylor Marr said in a statement.

Nowhere is that more obvious than in the Bay Area, where deep-pocketed buyers competing for homes amid a severe shortage have sent the median single-family house price soaring to $1.25 million, a 28% jump over the past three years, according to the California Association of Realtors. At the same time, average mortgage rates have doubled to more than 6%, spiking monthly payments by thousands of dollars.

Those rising costs mean that just one in five Bay Area residents can comfortably afford to buy a median-priced, single-family home, according to a recent report by the association. Nationwide, 40% of people can afford a typical home at the national median price of around $371,200.

A 1.25 million dollar median home cost, $11,000 mortgage payments. Those numbers are insane and will only accelerate houselessness.

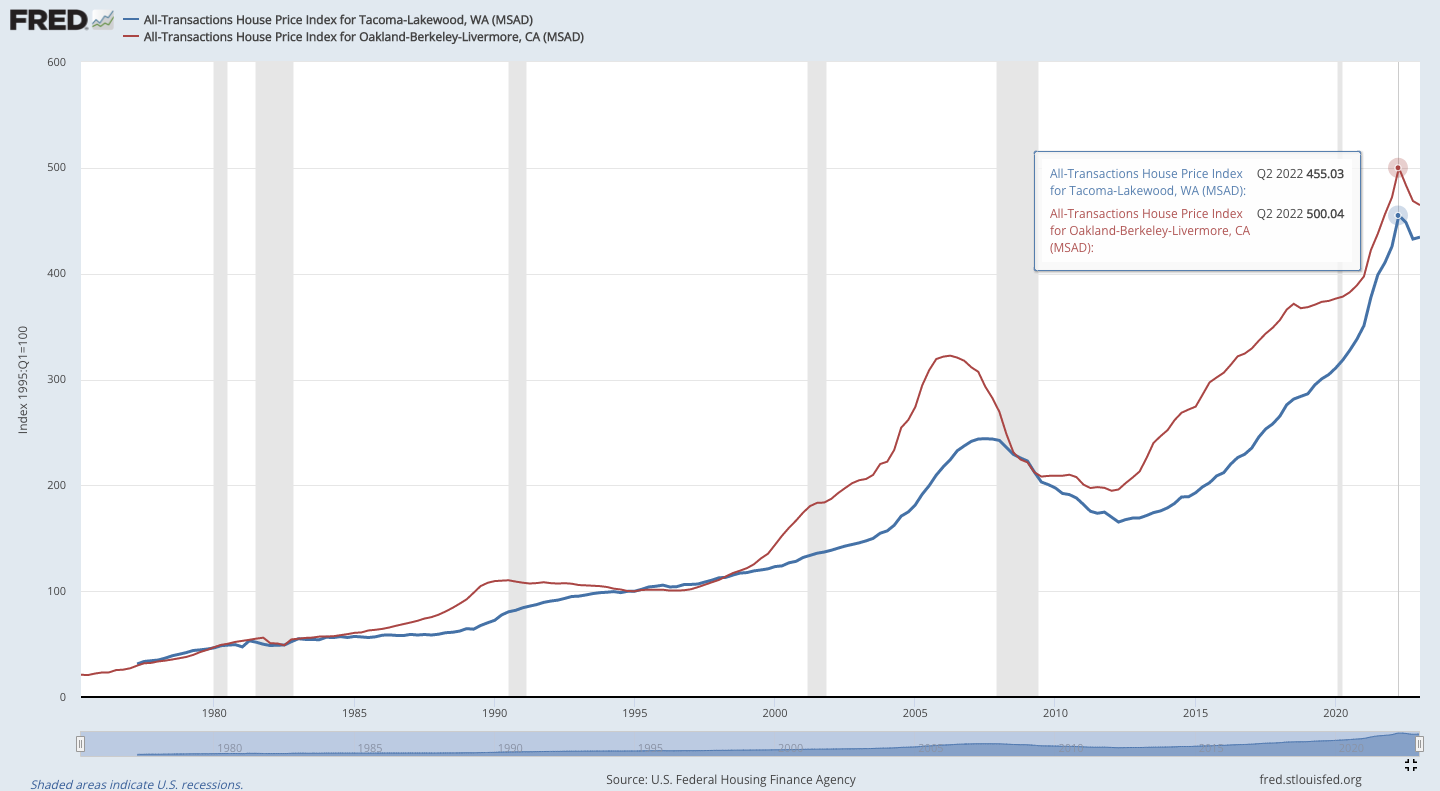

It’s easy to dismiss what’s happening in the Bay as a “California problem” but all the same inputs and many of the same bad policies are in place elsewhere. Above is data from the Saint Louis Federal Reserve. Home prices in Tacoma track the movements in Oakland but we’re headed where prices are there sooner than later. While the recently passed Middle Housing Bill in Washington State is a step in the right direction, it’s a drop in the bucket compared to the total demand that’s out here. We are essentially facing the comeuppance from forty years of bad policy and need a generational solution.

But I am not optimistic that we’re going to get one.

Recommendations and Bits for this Week

I think it's worth beginning this week's bits where we ended last week's newsletter. Over the last seven days several of you have sent me links to articles and examples of pig butchering scandals. One point that I under sold in my write-up last week is the relationship between the scams and cryptocurrency. Cryptocurrencies are essentially unregulated stocks and cryptocurrency exchanges as unregulated shadow banks. This means they have the ability to offer potential returns to investors that are far greater than traditional investment devices. However, that lack of regulation means they also are rife with scams.

Here’s an example, another of a mark from Reddit, you can tell as the person explains their story, they realize how naive they have been and cost themselves 36 thousand dollars. But an even more egregious example is this person who has been scammed out at nearly ten million dollars. We live in the Golden Age of both greed and grift.

Next, if I may appropriate a Fresh Prince analogy: when I started teaching in 2006, I was in my late twenties. Now I find myself in my 40s. I've gone from being Will to Uncle Phil. This week was graduation here in the Gulf. For pandemic reasons, I haven’t attended a graduation since June 2019 when I was still back in Tacoma. These are my babies. My first year here in Abu Dhabi, was their ninth grade year. I had the pleasure of watching them grow up and become (mostly) delightful tiny adults. Congrats to the class of 2023, (especially if you subscribe to the newsletter.)

Lastly, with this week's newsletter dedicated to housing, it's worth sharing this week's episode of the podcast. I interviewed organizers from Tacoma 4 All. They are a tenant lead group seeking to put an initiative to city voters to create a Tenant Bill of Rights. During the conversation, I put them through their paces on the silly moral hazard and freeloader concerns that have been raised and they dealt with them well. They will be hosting an in-person meeting on January 11th. If you are interested and can go you should tell them Nate sent you.

As always, thanks for reading the newsletter. If you'd like to opine just hit reply on the email. I welcome your feedback (especially if you think I am wrong about something) and if you like the newsletter, share it with somebody you love.

See you next week!