Music tech ownership ouroboros, 2026 edition

With DistroKid, Concord, Kobalt, and The Team (f.k.a. Wasserman) all up for sale, it’s time to revisit who owns what in music tech.

Hi there! Happy Thursday.

A few updates before we dive in:

First, thank you for the incredible response to my previous article, “AI music is on a collision course.” The volume of replies, shares, and constructive conversations it sparked has been pleasantly overwhelming. It’s clear that a lot of people in the industry are feeling the same way, and that there’s a strong appetite for thoughtful divergence. :)

Second, I'm going on a mini-conference tour this spring. If you're attending any of the following, I'd love to say hi:

SPOT+ in Aarhus, Denmark — giving a keynote on AI music trends and misconceptions

Music Biz in Atlanta — moderating a panel on AI labeling, designed directly around my article on the topic

Berklee’s AIMS (AI Music Summit) in Boston — serving as Program Co-Chair alongside Jonathan Wyner

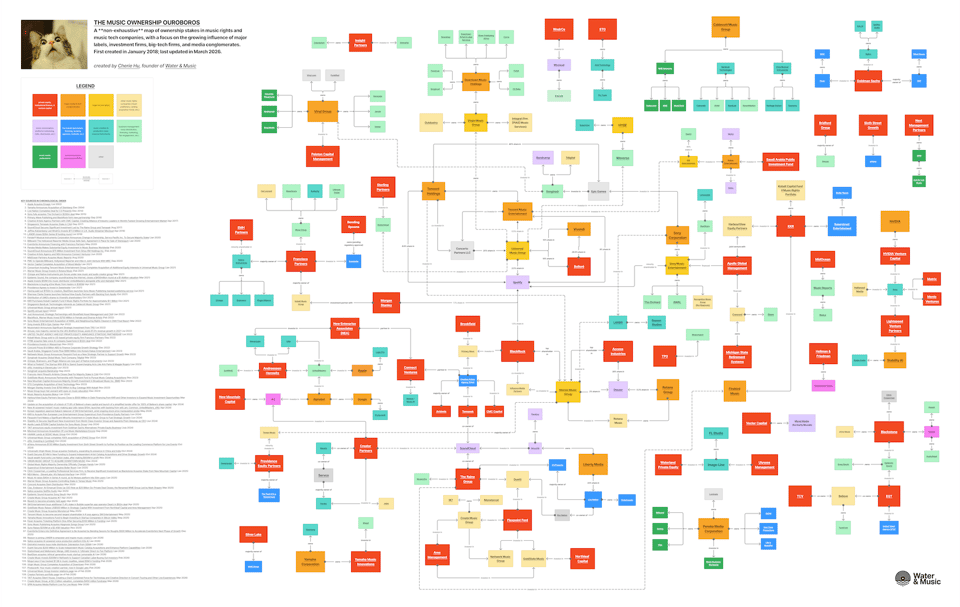

Today’s issue features a major update to Water & Music’s most popular market map, the Music Tech Ownership Ouroboros. The music tech market has felt especially chaotic these days, and I'm excited to walk you through everything that’s changed in the last year.

We’ve had over 500 new subscribers join us since the last issue. If you’re one of these folks, welcome! Feel free to reply directly to this email to introduce yourself — I read everything that comes through.

Thank you so much for your support!

Best,

Cherie Hu

Founder, Water & Music

Music tech ownership ouroboros, 2026 edition

You can also read this article via our newsletter archives or on LinkedIn.

I don’t know if it’s because of existential AI angst, post-COVID disillusionment, or the heaps of “dry powder” sitting on the sidelines, but music tech dealmaking is feeling particularly intense these days. New upstarts are fundraising in the same breath that they are getting sued; companies initially built to challenge incumbents are increasingly getting swallowed up inside them; and several longstanding institutions are suddenly up for sale.

Consider the following:

Downtown Music Holdings, one of the world’s largest independent music companies, now belongs to Universal Music Group, the world’s largest record label.

Hipgnosis Songs Group, once pitched as a radical alternative to traditional publishing, now sits inside Sony Music Publishing.

Native Instruments has entered preliminary insolvency, five years after its landmark private equity acquisition by Francisco Partners.

Concord and Kobalt, two of the world's biggest non-major publishers, are exploring sales to BMG and Primary Wave, respectively.

DistroKid, one of the leading indie music distributors, is exploring a sale for as much as $2B.

The Team (fka Wasserman) — the talent agency that booked the most artists for Coachella 2026 — is on the market amid fallout around owner Casey Wasserman's involvement in the Epstein Files.

The AI music market is consolidating quickly, with Google, Splice, LANDR, and BeatStars all announcing AI acquisitions in the last three months.

With this level of chaos, it’s a good time to revisit Water & Music’s longest-running market map, the Music Tech Ownership Ouroboros. The corporate deals listed above are just the tip of the iceberg of how power and ownership are rapidly changing hands in real time.

ICYMI: For the past eight years, the Music Tech Ownership Ouroboros has mapped the intricate web of financial investments and ownership stakes in music tech, with a focus on the growing influence of major labels, media conglomerates, big-tech companies, private equity firms, venture capital firms, and sovereign wealth funds.

I built this map because media coverage tends to treat "the music industry" as a singular, homogeneous entity, when in reality it’s home to a sprawling ecosystem of overlapping, often competing interests.

When you climb high up enough on the industry food chain, you find that significant parts of the music business are owned by a small handful of players — mostly outside of music. Some of these players co-invest with each other (e.g. Ares Management and Flexpoint Ford); in some cases, they even hold equity stakes in each other (e.g. Tencent and Spotify's 2017 equity swap).

All of this leads to the "ouroboros" nature of the market, where capital, ownership, and influence loop back on themselves.

The last major update I published to this Ouroboros was over a year ago, in February 2025. Today’s update adds 50+ new deals, leading to a total of 200+ distinct investment and ownership relationships on the board.

You can view a full changelog of new deals added here, or read on for my analysis of four high-level trends that emerged from this past year's wave.

An important note: This map isn’t exhaustive. For the sake of scope, I'm focusing primarily on growth-stage investments and acquisitions involving major corporate or institutional buyers. That said, if you Ctrl+F on the map, there's a good chance you’ll find your favorite music tech company.

1. AI music is consolidating quickly

AI music creation and production now comprise one of the fastest-growing categories on the Ouroboros. Whereas last year there were virtually no AI companies on the map, today we see Suno, Udio, ElevenLabs, Stable Audio, Moises, Supertone, BandLab, Lemonaide, LANDR, Kits AI, and ProducerAI all feeding into larger investment and portfolio plays.

Even though AI/ML as underlying technologies have been around for years, it was only in 2025 when “AI audio” as a standalone category emerged as a viable contender for growth-stage investments and M&A. Models improved drastically, which led to use cases becoming more apparent, which led to actual revenue growth from market leaders, with Suno and ElevenLabs each reporting over 50% growth in ARR in just six months.

So the capital has followed from all directions. We’re starting to see rival portfolios and theses emerge on AI music, in both venture and strategic funding circles.

Andreessen Horowitz and Lightspeed Venture Partners are neck-and-neck in the race to own foundational music models — with the former investing in Udio and ElevenLabs, and the latter backing Suno and Stability AI (maker of Stable Audio). a16z has also invested in UnitedMasters and [untitled], building out a holistic music portfolio that few of its competitors match.

Meanwhile, several industry juggernauts including CAA, HYBE, Warner Music, Yamaha Music Innovations, and the Sony Innovation Fund have all invested in or acquired their own AI tools, focused more on shaping granular creative workflows than on generating songs wholesale.

M&A in AI music has also been heavily workflow-focused so far:

LANDR acquired Reason, a DAW and plugin company

Splice acquired both Spitfire Audio (a leading sample & virtual instrument library) and Kits AI (an AI-powered voice production platform)

BeatStars acquired Lemonaide, a startup focused on MIDI generation for producers

Google acquired ProducerAI and relaunched the product under Google Labs

In our previous article on the AI music collision course, we dubbed this convergence the “DAWification” of everything. If the products, features, and workflows converge, it follows that to some extent, the business must also converge. No wonder so many investors want a slice of this pie right now.

2. Live music grows as a complement, not competitor, to AI

Right alongside AI, live entertainment has emerged as a particularly active category in this Ouroboros update.

The timing is perfect, as live is at the center of one of the biggest industry stories of 2026 so far: The U.S. Department of Justice reached a surprise settlement with Live Nation this week, allowing the company to keep Ticketmaster rather than forcing a divestiture. I won’t go into the details of the settlement here — many peers have published excellent takes elsewhere.

The point I want to make is that there’s a wider trend outside of Live Nation: For years, live events have been experiencing their own version of the financialization and consolidation that previously swept through the recording and publishing businesses.

If you watched Rihanna’s Super Bowl halftime show, the Backstreet Boys’ Sphere residency, or recent tours by Taylor Swift, My Chemical Romance, Tate McRae, and Dua Lipa, you indirectly have Goldman Sachs to thank for the production value.

In July 2024, Goldman purchased a majority stake in TAIT, a prolific event production company that has developed experiences for all of the above artists. On March 2, 2026, TAIT then announced their acquisition of Silent House, another creative production company that worked on Taylor Swift’s Eras Tour, Kendrick Lamar and SZA’s Grand National Tour, and Tyler, The Creator’s CHROMAKOPIA tour.

Some other recent highlights:

Fever, a ticketing company that also counts Goldman Sachs as an investor, acquired competitor DICE in June 2025. DICE had previously raised a $122M Series C led by Softbank.

KKR's portfolio company Superstruct Entertainment acquired Boiler Room from DICE in January 2025, bringing one of the most culturally influential live music brands under private equity ownership.

Saudi Arabia's Public Investment Fund exited its Live Nation stake in November 2024, after making $930M in profit.

Bending Spoons acquired Eventbrite for roughly $500M in December 2025 — a rare example of a tech-first acquirer moving into live events.

Sixth Street Growth invested $130M into the live commerce platform atVenu in October 2024.

The news that The Team (f.k.a. Wasserman) is for sale also illuminates the fact that nearly all the top talent agencies are majority-owned by private equity firms or family offices: The Team by Providence Equity, CAA by Groupe Artémis, and WME by Silver Lake. UTA is minority-owned by EQT, which is also an investor in Believe and Epidemic Sound.

Private equity involvement is a relatively new phenomenon in the agency world, with all of these transactions taking place within the last five years. Providence has said that it remains “fully committed” to investing in The Team, despite the recent turbulence.

Whether or not the Live Nation settlement sticks, I think we will see VCs and private equity firms continuing to bet heavily on IRL experiences as a major growth frontier. In fact, there’s a strong case that AI-driven software and IRL live experiences will actually grow in tandem, as complementary rather than competitive forces.

Young people are both more likely to lean into AI-generated music and, ironically, more likely to log off. Event-centric brands like Breakaway and 222 have raised fresh VC rounds in the last few months. And in music, labels are increasingly experimenting with immersive IRL fan gatherings — e.g. album-themed parties, exhibitions, and city-wide activations — that foster fan communities around an artist’s world, even when the artist is not physically present.

In other words, as music creation becomes easier to scale digitally, the scarcest commodity in the business may become the experience of being physically together.

3. The rights power play moves to data & infrastructure

In every industry, every problem can trace back to a meta-problem that dictates everything else.

For music, that meta-problem is metadata — i.e. data about who owns what. Whether you’re trying to license an opt-in catalog for AI deals, clear tracks for a micro-sync on TikTok, or simply determine who should get paid, many of the industry’s most pressing challenges break down without clean metadata.

That's why the rights corner of the Ouroboros, as traditional and slow-moving as it may seem, is critical to follow.

Ever since the Ouroboros was first published in 2018, major labels and publishers have been at the center of power on the map. They built their influence not only by buying up other labels or catalogs and folding them in, but also by purchasing equity stakes in infrastructure across streaming services, distributors, and services companies. UMG is unsurprisingly one of the top movers here, owning Downtown Music (via Virgin Music Group) and holding equity in Spotify, Weverse, and Stationhead.

Beyond the majors, however, a new generation of rights-focused companies are taking a different approach, combining IP ownership with deliberate investment in modern data infrastructure to manage those catalogs more effectively.

Create Music Group has undergone a significant restructure in the last several years — from a primarily tech-focused music brand, with tools like Label Engine and Yoon, into a proper label owner and operator in its own right. In the last year alone, the company acquired reputable indie labels !K7 and Monstercat, invested $300M in Nettwerk, and completed a $450M fundraise at a $2.2B valuation. With the switch to focus on IP, Create seems to be pursuing a similar strategy to Firebird in the management world: Acquire complementary labels and catalogs, then build an internal tech stack that can serve all of them, driving down operational costs.

Similarly, Duetti has raised over $300M from the likes of The Raine Group and Flexpoint Ford, on the thesis that indie catalogs are systematically undervalued and that better data infrastructure can unlock that value. As Billboard reported, their approach is less about aggregating rights, and more about providing the kind of hands-on management that small catalogs have historically lacked. Duetti also recently collaborated with Billboard on the inaugural Music Finance Index, with the goal of establishing a public benchmark on catalog multiples across genres and geographies.

Songtradr has spent the last several years assembling one of the most vertically integrated music-service stacks in the market, spanning sync licensing (Big Sync), sonic branding (MassiveMusic), metadata (Musicube), enterprise music delivery (7digital), and direct-to-fan commerce (Bandcamp). They’re valued at roughly $1B today, and, unlike the other companies in this section, face the immense challenge of integrating very different businesses into one operationally coherent holding company.

The next phase of the rights business may be less about who owns the most music, and more about who owns the systems that organize, price, and activate it.

4. Specialized investors are building distinct theses on music tech

Lastly, one of the most interesting new dimensions of this update is the number of specialized investment firms now visible on the map. While their portfolios often overlap, their strategies tend to cluster around different parts of the music value chain, from financial infrastructure to creator ecosystems and workflows.

The Raine Group is one of the most influential players in music tech investment that you might not know about if you’re not working directly in finance. Their music portfolio spans virtually every part of the business, including DSPs (SoundCloud), catalog acquisition (Duetti), artist management (Firebird), live events (C3 Presents), and rights management (MusicInfra). Beyond investment, they also advised Stem on its sale to Concord, and are currently advising on the DistroKid sale.

Creator Partners, led by Kerry Trainor (former CEO of SoundCloud and Vimeo), sits closer to the creator-economy side of the market, with a thesis that durable creative identities require tools, communities, and platforms that sit upstream of distribution. Alongside stakes in companies like BMI and SoundCloud, Creator Partners is also one of the few investors on the map with meaningful exposure to music hardware and instruments, including positions in Fender and Reverb. Even amid the surge of AI tools, there remains a strong case for physical instruments and gear, as part of a broader cultural swing toward tangible media and in-person creative experiences.

Yamaha Music Innovations, which launched in May 2025 as the investment arm of Yamaha Corporation, aims to extend Yamaha’s role across the digital creator stack beyond just instruments alone. Their team brings together industry veterans from across music and tech, including longtime Yamaha exec Scott Yusuke Sugino, Managing Partner Andrew Kahn (formerly of Crush Ventures), and Senior Principal Conor Healy (formerly of Jen Music AI and SB Projects). They are also one of the few specialist music tech funds to have a newsletter; their recent essays including “The Creator's Stack” and “The T-Shirt Test” make clear how the team is interested not just in new apps, but in the wider ecosystems and identities shaping the lives of both artists and fans.

For founders and industry operators, understanding these portfolio strategies reveals something essential about the investor on the other side of the table — not just what they fund, but what future of music they believe they are building.

So what?

The ouroboros will keep growing. If the first months of 2026 are any indication, the cycles will also keep accelerating.

In this landscape, I believe the Ouroboros is best understood not as surface-level corporate gossip, but as a deeper signal map.

While capital may appear to move chaotically, it rarely moves randomly. Over time, it clusters around the parts of the value chain that investors believe will control the next decade of music. This year’s update makes those clusters especially clear, across AI tools, live experiences, and rights data infrastructure.

Tracking who funds what — and why — can reveal as much about where the industry is heading as the technologies themselves. Read through that lens, a few strategic questions emerge for anyone building in music tech:

Where does your roadmap sit in someone else’s portfolio strategy? Many investors are no longer funding standalone products, but assembling wider, comprehensive ecosystems of tools and services.

What infrastructure layer are you actually building on? Whether we’re talking about distribution, rights management, ticketing, fan data, or AI models, direct ownership of infrastructure increasingly determines who captures value.

The challenge in this environment is not simply to innovate, but to understand where your work sits inside a much larger web of capital, ownership, and incentives. In an industry where music companies are constantly being folded into larger portfolios, the real strategic question becomes: Are you building a business — or a piece of someone else’s system?

You can view a full changelog of new deals added to the map since our last update in February 2025 by clicking here.