Why You Should Monitor Your Property Details Online

Did you know that details about your property are available online to anyone?

Not just realtors with MLS access, but anyone in the general public can access things like your property deed, your tax card, and certain details about your mortgage history. Periodically doing a quick check on these records is good practice for anyone.

Deeds Search

To access your deed, go to your county’s register of deeds office online. For instance, in Forsyth County, go to the Register of Deeds site, where you'll search using your first and last name. (Deed searches are always tied to name, as opposed to tax searches, which are tied to property address.) In the deeds office, you can pull up your property deed as well as any deeds of satisfaction (such as when your home loan is paid off and your lender has released you from the debt). You can also access things like quit claims, free trader agreements, easements, powers of attorney, and any financial encumbrances associated with a property.

For the sake of caution, I’d recommend you also set up a fraud alert here. Though rare, home title fraud does occur, and when it does it’s catastrophic. You can’t always anticipate fraud or defend yourself against it, but there are some measures you can take to monitor and safeguard your interests.

First, check your property records regularly (I check mine once every month or two).

While you’re there, set up a Property Fraud Alert or Property Check service. These are pretty easy to locate and activate on your municipal website. If, after activating, you are ever alerted by the system, take action immediately.

For instance, to activate Forsyth County’s fraud alert system, go to https://www.co.forsyth.nc.us/rod/.

Title insurance comes in handy here, as well. Your title insurance policy, which you purchased when you purchased your home (your lender or your closing attorney should have taken care of this and built it into your closing costs), will hire and pay for an attorney to help you defend your property rights. It’ll cover court costs and all other costs associated with the fraudulent claim. So, if given the choice, never skip title insurance. More to come on this in an upcoming newsletter.

Tax Information Search

To access your tax information, go to the tax assessor's website for the county where your property resides. Your tax card, which you search by property address (instead of by your name, as in the case of the deed search) offers tons of information. In addition to things like property description, zoning, acreage, HVAC, and foundation type, you can access details about the land value and building values, as well as the value of improvements you’ve made to the property.

Another interesting feature the tax card offers is year-built versus effective-year-built—this gives the actual year the house was constructed compared to when it may as well have been constructed due to updates you’ve made. So a home built in 1950 with a new kitchen and bathrooms renovated in 2020 might have an effective-year-built date of much later than 1950.

Checking your tax card is not necessarily something you need to do regularly, but where it is and how to get there can be helpful, especially in reassessment years. And it’s always interesting to see how your municipality quantifies the features and value of your home.

Hopefully this is useful, pertinent information for my readers. As always, don’t hesitate to shoot me a line about anything you’d like me to present in future issues. No question is too small and no topic is too big. Thanks for your support.

Best,

Robin

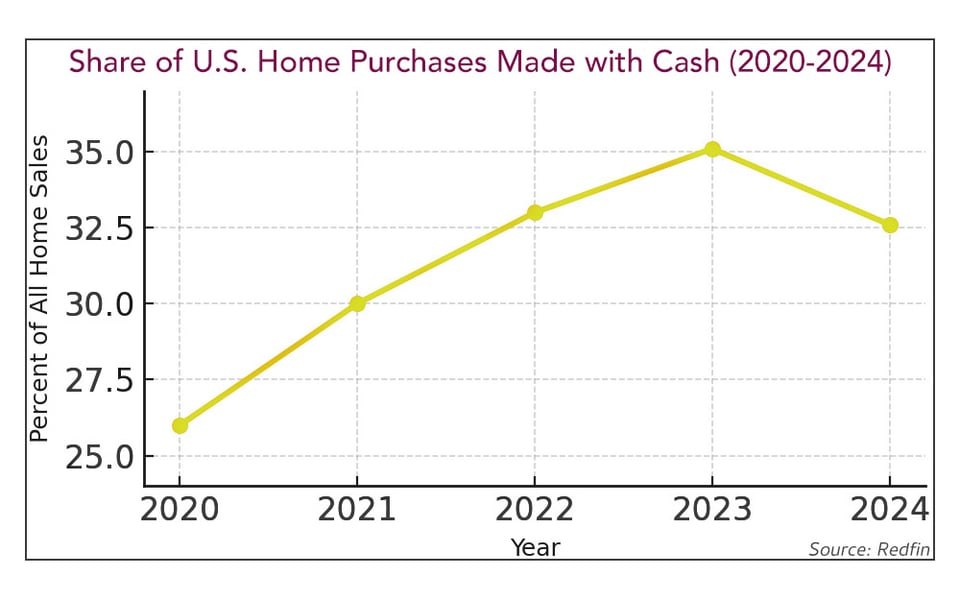

October’s Cupcake: Cash Buyers Still in the Game, but Losing a Little Ground

In recent years, cash buyers have played an unusually large role in the real estate market. But that gap may be starting to narrow.

In 2024, just under one-third of U.S. home buyers paid in cash, down from 35.1% in 2023. That’s the lowest share since 2021. Cash sales were as low as 26% during the pandemic.

Some housing experts believe the housing market is finding balance again. Investor demand has cooled, more homes are hitting the market, and mortgage buyers are reappearing after being priced out by high rates.

Affordability is still tight, but the days when cash buyers routinely outbid everyone else may finally be fading.

(Sources: Redfin, Realtor.com, National Association of REALTORS®, Investopedia, GlobeSt.)