Title Insurance & You

What it is, what it’s not, and why you need it…

Though not the sexiest of real estate topics, title insurance is one of the most important to understand. It’s also one of the most misunderstood.

As the name indicates, title insurance is a type of insurance policy that protects against unknown or hidden defects in a property’s title at the time of purchase. Such defects might include errors in public records, improper recording of past deeds, boundary or easement disputes, forgery or fraud in past deeds, or failure on the part of former owners to pay taxes or mechanics liens tied to the property.

Other forms of insurance (like health, car, or homeowners) protect against future events, but lender’s insurance protects against the past. It covers legal fees, settlements, and any related financial losses incurred by the policy owner in the event of a claim against the property. And, unlike other policies, title insurance only requires a one-time payment, not a recurring premium.

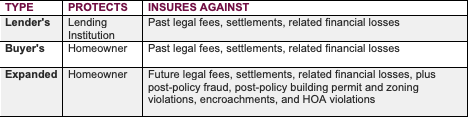

It’s important to note that there are three types of title insurance policies, each of which covers different parties. These are lenders, owners, and expanded.

Lender’s Title Insurance is required by lenders and protects lenders exclusively; it does not protect the homeowner. If you are financing your home, your lender will require you to buy this policy as part of your closing costs. As the principal owed on the property decreases, so will the lender policy coverage amount. Once the loan is paid off, the lender’s title insurance policy ceases.

Owner’s Title Insurance, on the other hand, isn’t required by any state law or institution, but it’s strongly recommended. This policy protects you, the homeowner, for as long as you own the property. It’s always a good idea to purchase this whether financing your home or buying outright in cash. Owner’s title insurance is so valuable, in fact, that in several states, sellers customarily offer to pay for it as a way to sweeten the deal for buyers.

ALTA Homeowners Expanded Title Insurance Policy, the gold-standard for homeowners, protects you against future title issues, affording broader coverage than the standard owner’s policy and protecting against risks that may arise after the property purchase. In addition to standard protections, it adds coverage for issues like post-policy fraud, post-policy building permit and zoning violations, encroachments, and HOA violations. Not only that, it embeds inflation protection, automatically increasing the policy's coverage amount (up to a certain, initially stated percentage) as the property appreciates over time. Who wouldn’t love this?

Knowledge = Security

Many people hear the term “title insurance” and assume it's a good thing for them. Because it's insurance, they don't explore any further. But it’s imperative that homebuyers understand the types of title insurance available and who and what is protected by each. Armed with this knowledge, you can better ensure that your home and all the equity you have tied up in it are safe.

Check with title insurance companies in your state to confirm rates and protections. As with anything else real estate-related, speak to your realtor or real estate attorney with any questions you may have.

Key Takeaways

Ask your real estate broker to recommend some title insurance companies, then take a moment to contact each for policy options and rates.

In tight negotiations, discuss with your agent the possibility of requesting seller-paid owner’s title insurance. This can be a nice perk for buyers.

👍 Big thanks to Meredith Galloway, Business Relationship Manager at Cardinal Title Center in Brevard, NC, for her expert help. If you have a question for her, please let me know and I'll introduce you.

Best,

Robin

November’s Cupcake: Inventory is Up—What it Means

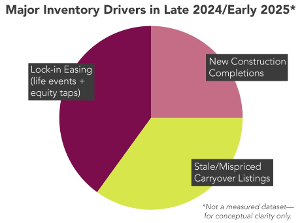

Inventory in Winston-Salem and Greensboro is ticking higher. Not dramatically, but noticeably.

There are a few reasons.

First, the lock-in effect is loosening. Some homeowners with low 2.75–3.50 percent mortgages from 2020–2021 (pandemic refinancers as well as those who purchased during that timeframe) are now confronting costly life events—job changes, caregiving, divorce, downsizing, estate transitions. For them, necessity often overrides rate-sensitivity. The financial penalty of trading three percent for seven percent hurts, but some simply can't defer the decision any longer.

Second, builders are finally delivering product that was delayed during the 2022–2023 supply-chain bottlenecks. New construction completion rates have improved, and that's showing up in Forsyth, Guilford, and Davie County listings. It's not a flood of volume, but it is real, incremental supply.

Third, some current inventory is simply stale listings. Price expectations set in 2021 still creep into today's asking prices, and when a home is misaligned on price or condition, it just sits, inflating the active-listings number even when new volume remains moderate.

What to Expect Near-Term

December is typically the lowest-velocity month of the year for showings, contracts, and buyer activity. The market doesn't fully reengage until the second half of January, and that will likely hold true again.

Once we get 2026 up and running, though, buyers should find selection improving and negotiating position strengthened. For sellers: realistic pricing, staging, and curb appeal matter more than ever. A clean, well-supported list price is now a strategic advantage.

Sources: S&P Case-Shiller; Mortgage Bankers Association; National Association of Home Builders; Triangle MLS and Triad MLS year-over-year days-on-market summaries.