Uncertainty

Hello!

Our recent preoccupation with LNG has been realised in a new Polycrisis / Phenomenal World essay. This fuel has the allure of versatility and modernity, but the misfortune of its ascent coinciding with that of attractive alternatives. That creates a kind of intrinsic uncertainty that makes it harder for countries, and even some companies, to tolerate the bumpy trajectory of price spikes and gluts that is inevitable in a new commodity market with a relatively complex, capital-intensive supply chain. This week, The Dig published the second part of the conversation with Tim and Ilas Alamy, covering.a lot of core Polycrisis topics.

- Kate & Tim

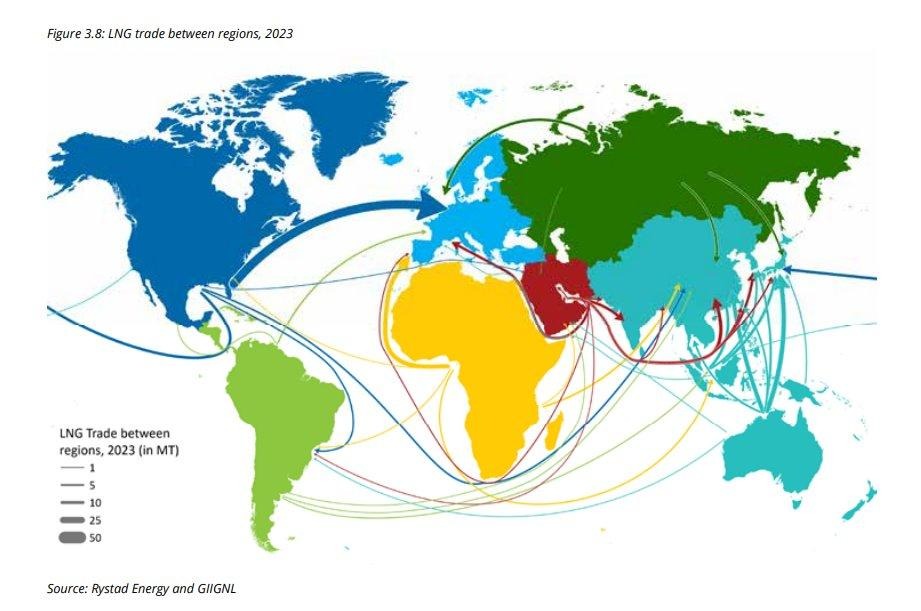

LNG: The fossil fuel of the polycrisis

Our theory is that while oil came of age slowly (it was a different era after all) it was also inexorable; it was necessary for what then was the dominant mode of providing energy for transport, and substitution was difficult. The built equipment – not just cars and other vehicles, but the factories and workforces that made them – created path dependency. Oil was inevitable, so investing in the infrastructure to enable it was a unidirectional bet. Despite its volatility and other disadvantages, most countries didn’t seriously explore alternatives (although Japan and Brazil certainly did).

For methane though, it’s different. Sure, fossil gas is flexible, suits electrification and can be burnt in power stations that are relatively easy to build – but it can also be easily substituted. That makes it harder to tolerate the incredible swings in prices to supply chains and production that are occurring thanks to wars, droughts and other upheavals.

Today’s LNG markets in theory make it a steadier prospect; deep, liquid, more international. It makes hedging easier. But more than half of LNG is bought and sold under bespoke contracts of up to three decades. In less than three years, Pakistan has gone from blackouts when its shipments were diverted to Europe, to desperate unsuccessful bids for new LNG shipments, to an LNG glut. The country is no longer counting on LNG as a key source of energy.

The US oil and gas industry is having its face-eating leopard moment

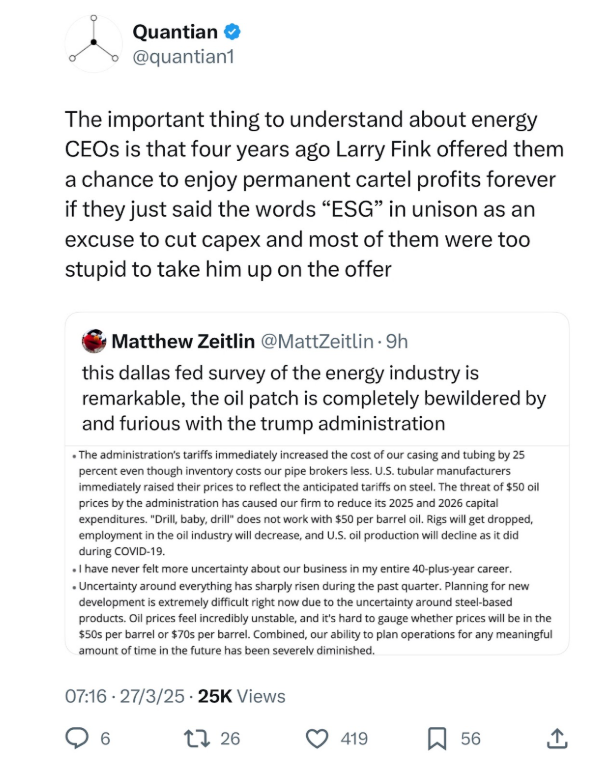

The Dallas Fed surveys executives from a couple of hundred oil and gas companies every quarter. The latest survey, conducted in mid-March and published this week was… dire. Tracy Alloway at Bloomberg’s Odd Lots wrote:

To sum it up, the survey is bad. It’s really worth reading the whole thing but to sum it up, it’s full of anonymous energy executives complaining about how the new Trump administration is creating massive uncertainty for their business viz the back-and-forth on tariffs.

But the survey is also instructive when it comes to highlighting some big truisms of the oil business.

Here’s what caught my eye:

Cost of components:

“The administration’s tariffs immediately increased the cost of our casing and tubing by 25 percent even though inventory costs our pipe brokers less. U.S. tubular manufacturers immediately raised their prices to reflect the anticipated tariffs on steel.”

Yes, this was an industry that supported the Trump campaign.

Tracy goes on to point out that a particularly painful aspect of the tariff-related chaos and dread for oil companies is that the actual components that they rely upon to make their operations more efficient are also affected. So there isn’t an obvious way for the industry to deal with the new price pressure.

Perhaps the best take on this:

Certainty matters

Aside from the oil patch sentiment, another piece of data that began to look negative was US business equipment orders, which fell unexpectedly in February.

Something most people working at the interface of policy and business will hear a lot is that business wants “policy certainty”. This phrase is ambiguous enough to be used in support of a specific policy. But, it turns out, the phrase is also true – and not just for, say, climate change (which is how I came across it). The tariff travails of the oil and gas industry extractive industry are an example.

There’s some examples in the methane gas sector, too. A couple of years ago, LNG tankers production was booming — they were on track to outnumber oil tankers by 2028. Now there is, wait for it, a glut of LNG tankers.

Meanwhile gas turbines – required to burn that LNG – are on back order through to 2030, and two of the three companies that dominate gas turbine manufacturing have said they have no intention of expanding their pipeline, and are even contemplating auctioning off spots higher up in the queue. Far from a perfectly competitive market, then (but what market is?). Advait Arun explained this reluctance to expand in Heatmap earlier this year: it comes from a lack of certainty that, ironically, was driven home for turbine makers from their experience in the wind power industry:

These gas turbine manufacturers are also some of the world’s leading wind turbine blade manufacturers, and a similar fate befell that sector in the past decade. Large-scale capacity expansion and competition for contracts drove down costs and margins across the supply chain — only for those to move sharply in reverse when supply chains froze up during the pandemic and interest rates shot up in 2023. Now offshore wind projects are plagued with problems and, at least in the U.S., President Trump’s de facto moratorium on offshore wind development has further reduced the sector’s ability to bounce back. These companies have been burned before. It only makes sense not to repeat past mistakes.

Business academics who study uncertainty effects on business investment have a lot of new case studies in the pipeline.

Some things we’re reading

Mona Ali’s new essay on Suez, sovereignty, energy and debt.

Tariffs: Carbon Brief’s guide, featuring many experts inc Tim and Bentley.

New World Order: Tim and Ilias Alami on The Dig, Part 2

There’s a Wages of Destruction book club on the Odd Lots discord, and Adam Tooze is popping in.

The dollar’s future: Barry Eichengreen, last week, had a long essay in the FT about the history of, and possible end of, dollar centrality. Bloomberg, yesterday, on signs that the dollar is already losing its safe haven status.

There’s an election in Australia, and Alex Turnbull is unpacking associated energy disinformation.

See you next week!

Add a comment: