The era of real energy security has arrived

Dear readers,

The podcast has landed! We made it with Sarah Allely and we are so pleased. You can hear at (Apple), (Spotify), Overcast, or wherever else you want.

We wanted the podcast to give a more accessible overview of the very complex area of energy transition and geopolitics. Although most of it was recorded before this Middle East war, the overlap between energy transition and energy security has only become more obvious; especially in Asia. Please share it with your normie friends.

Episode 1 introduces the new wave of China-enabled energy transition - with Haneea Isaad from IEEFA in Pakistan telling us about the speed of solar deployment there; and Kyle Chan from Brookings and “High Capacity” explaining why China does it.

Episode 2 Mark Blyth talks us through the dollar-energy connection, and then we hear from Naa Adjekai Adjei, an expert on Chinese energy finance in Africa, about these constraints play out in Global South countries with low energy access.

Both of us were just on the excellent This Machine Kills podcast, where we had a fun chat with Edward Ongweso Jr and Jathan Sadowski about some of our favourite topics (go subscribe to it, if you don't already - they explore many similar themes to us, with more of a tech bent).

Future episodes feature Helen Thompson, Alex Turnbull, Jessica Chen Weiss, Rhiana Gunn-Wright, Jake Werner, and Ted Fertik.

Oh yeah – we also have our own website! You can still get all our monthly Phenomenal World essays in the same place, in the same newsletter – but they'll also be here; along with all our other stuff.

You can email us here (Tim, Kate, all of us) and check out the Discord.

The oil narrative

One angle in the podcast that we did change slightly, as a result of the war, was the idea that the US military adventurism is partly motivated by a desire to emphasise, project and maintain the importance of oil.

In January, it seemed plausible that the US administration was – at least in part – trying re-assert the importance of oil as a narrative. The decapitation in Venezuela was, Trump insisted, largely about oil. But this made no sense; remember, Exxon and other international oil companies are unenthusiastic about going back into high cost, high risk Venezuela.

So was it more about the illusion of fossil-fuel based control? For decades, or really even more than a century, hegemons have threatened to either their adversaries cut off the supply to fuel sources, or to cut off the ability to sell them (Helen Thompson talks about this in episode 3 of our podcast, out in a few days). But even a gradual decline in oil demand means that being a keeper of oil flows no longer holds the same power. Oil markets are finely balanced; shifting from a small undersupply to a small oversupply has a big price effect. While companies can, to a degree, respond to this by adjusting investment plans or even production, it's tougher for highly dependent petrostates: Saudi Arabia, for example, had last year given up on trying to keep oil prices high and instead started ramping up production to sell while it still can. (Kate wrote more about this in a recent edition of The Break Down).

But does cutting off a fifth of the world’s supply of crude oil support that hypothesis? In the short-term, it raises export income for US oil and gas producers; this can be seen especially with US LNG exports. But it also raises domestic prices, raises prices of (needed) crude oil imports. In the longer term it’s the kind of strategy that is self-defeating - creating profound volatility and insecurity and intermittency - that militate against investors, consumers and governments alike

Okay, the longer term is clearly not a concern. To date, crude oil futures prices can be pushed around with Truth Social "mission accomplished!" posts. Those prices alone do not determine how countries make decisions about energy. No country that imports oil or LNG will think about energy security the same way after this. As one of our guests, Alex Turnbull, says in episode three (again: out next week!): energy crises are a bit like famines: once experienced, they are not easily forgotten. That degree of deprivation influences future decisions.

The era of real energy security is here. The commodities expert Nick Birman-Trickett wrote from CERAWeek - "Those who insist on promoting “pragmatism” are fighting the last war. They cannot fathom that the prime drivers of clean energy adoption are economics, speed, flexibility, and innovation, not ideology.... Power that’s cheap to install, quick to deliver, and increasingly cheap to hedge and manage is pragmatic. Chasing financing worth over $10 billion for an import-export terminal whose costs compound between infrastructure, supply contracts, and new levels of geopolitical risk doesn’t look so pragmatic."

Demand destruction, part I:

So what are countries experiencing this shock going to do? The main thing is cut dependence on imports on gas and oil, because they can be relatively easily controlled or disrupted by unreliable states and the loss of US naval supremacy over the world's oceans.

This is going to be a tough time for energy importing states, even those that can outbid others for shipments. Energy systems do not change quickly, so the effects will play out over months and years. But already there are signs of big investment and policy decisions responding:

Indonesia: electrification [from Argus]:

"This is a wake-up call," Indonesian president Prabowo Subianto said last week, in a call to push for electrification and renewable energy. Indonesia aims to have 100GW of solar power in "no later than two years", up from its current 11GW, he said, with earlier plans including battery energy storage system (Bess) deployments.

"We will convert all motorcycles into electric motorcycles. All cars, all trucks, all tractors must [also] be electric," he added.

Vietnam: cancelling LNG power? From Reuters, a story about Vietnam's largest conglomerate:

Vingroup has told Vietnam's government it wants to ditch a plan to build the country's largest LNG-fired power plant and embark on a renewable energy project instead, as the Iran war has boosted the risk of the fuel becoming too expensive, a document showed.

South Korea: smashing that Renewables button President Lee Jae-Myung, via Chosun Daily:

“The world is in turmoil right now because of energy issues. It’s a situation so serious that even I can’t sleep.

"South Korea needs to transition to renewable energy quickly. If we rely on fossil energy, the future will be extremely risky."

Enthusiasm for Chinese solar, batteries, electrolysers and EVs – already doing pretty well - will surge. The problem was always too-low demand rather than too little factory supply of green products. Its here that the oil crisis helps with surging consumer demand for cleantech.

Data for China’s March cleantech exports won’t be available for a few weeks, but anecdotes and reportage suggest something will be visible. For example, electric vehicle sellers are seeing cars moving much more quickly. Tim highlighted that in India, a shortage of LPG led to a run on portable induction cooktops.

Tim was featured in a NYT oped by Jonathan Mingle that argued that this is the first oil crisis in which alternatives to oil and gas — solar panels, EVs, batteries, induction stoves heatpumps — are cheap and easy to get, and so instability is leading to an epic surge in consumer demand.

Tim’s Bluesky thread has been collecting examples. Contribute your own using #DemandDestructionWatch.

Crowdsourcing electrotech surge in Iran war! lets use #DemandDestructionWatch BYD is now doing a fortnight's worth of sales each day "Wang singled out markets such as Australia,New Zealand.., where he said daily sales volumes are now as high as what the carmaker could previously sell in two weeks"

— Albert Pinto (@70sbachchan.bsky.social) April 04, 2026

Demand Destruction, part II: Why the oil industry hates high prices

The Break Down essay that Kate wrote seeks to explain exactly how Saudi Arabia hates prices that are too high, as well as too low. The reason is that Saudi Arabia is acutely aware of how sustained high prices lead to a reduction in oil consumption. When they talk about “stability”, they are talking about a price ceiling, rather than just a floor.

It’s not just petrostates with a high fiscal breakeven price who fear high prices. Other producers with high dependency and/or high production costs will see it, too. Axios reported the mood at CERAweek, the big annual hydrocarbon conference in Texas, as rather downbeat. “Instability is the defining mood”, Amy Harder wrote, and added that ConocoPhillips chief executive Ryan Lance in a main stage plenary described the market vibe as "a bit unstable," with a “subdued chuckle” “That nervous laughter felt like a mask for the deeper uncertainty permeating the conference.”

And even small US shale drillers hate the higher prices. FT story plainly headlined "why US shale oil producers are not cheering $100 oil" reveals that many don’t see it as a signal to drill more because they are not confident that they will remain at such levels. Ironically, some of the interviewed oilmen believed prices would fall back quickly because they were so confident in Trump's ability to quickly subdue Iran.

And then there is just volatility: another FT story looks at paralysis in US oil and gas dealmaking, citing an M&A person saying "everything is in paralysis right now because no one can price anything". One of the standard lines in climate policy advocacy is that business likes certainty; it's actually true.

There’s a commodities markets adage that “the cure for high prices is high prices”. In other words, high prices incentivise more investment in production; and then that increased production brings prices down. But that doesn’t work when the prices are so high that a shock is likely to reverberate in the same way that 1973, 1979 and less well-known shocks have done: cutting demand by substituting other fuel sources for oil, mandating energy efficiency, and big changes to the automotive industry (fuel efficiency doubled in the decade after 1979; and the consequences for the US car industry were so bad it is known as “the Malaise era”).

Why are oil prices still so low? Hubris, Information, and Timing

We and almost everyone else it seems have been asking this question: why did oil hang around the $100 mark instead of shooting up towards its all time high of $147 (which is actually more like $220 if adjusted for inflation)?

There are many theories but mostly they come down to an optimism about the prospects of the US ending the war or opening the Strait of Hormuz for all energy traffic; and the US economy's ability to withstand ongoing blockade of Hormuz.

A possible contributing factor is a simple inability to model the scenario at all. Alex Turnbull explained in detail something he’s been telling us about for years: it is POSSIBLE to model chokepoints and disruption to energy markets; but no-one is really doing it. An exception is people like Jun Ukita Shepard and Lincoln F. Pratson.

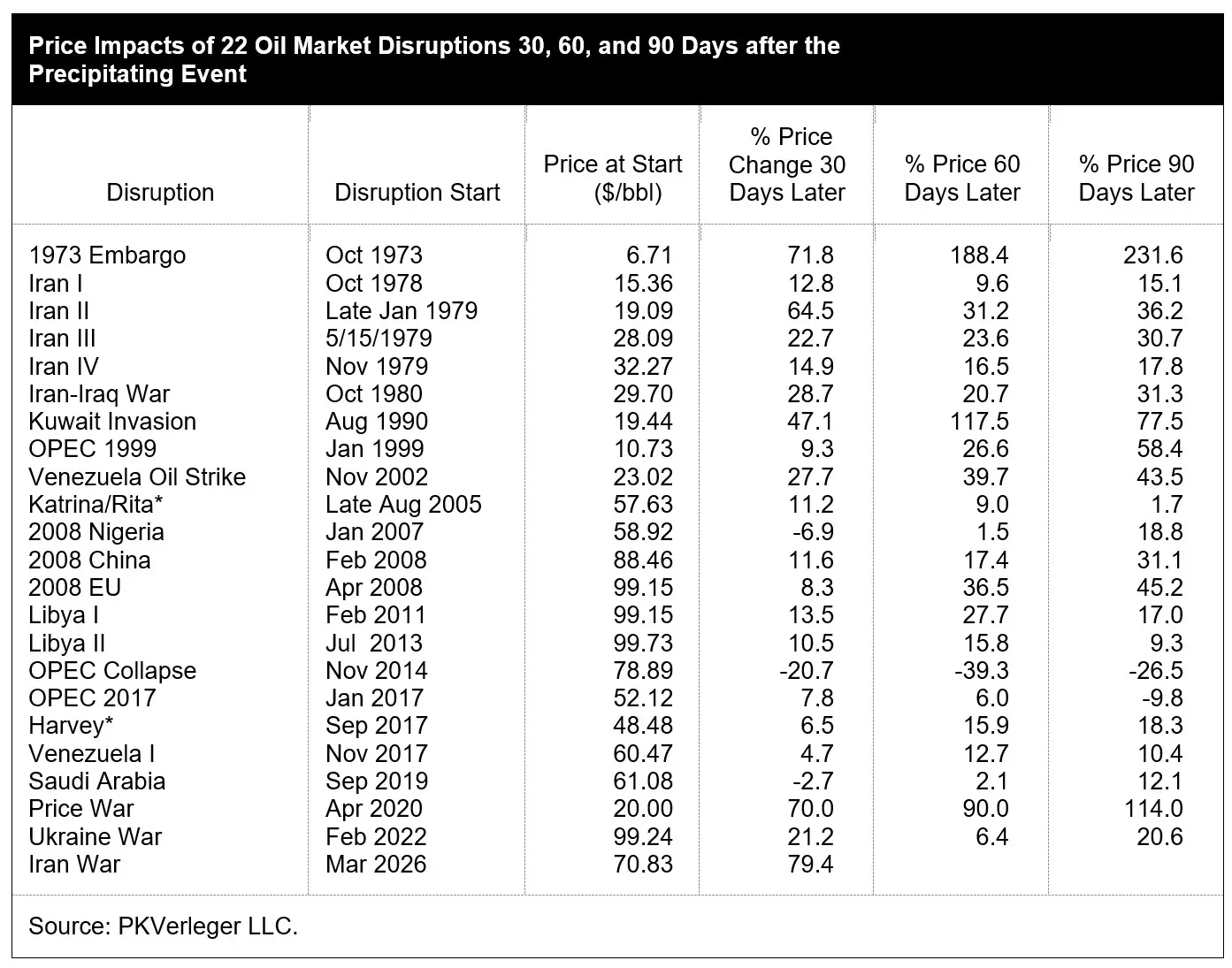

Phil Verleger calls it a “risk premium” that hasn’t existed before.

Verleger has also made a very cool comparison of changes in oil prices 30, 60, and 120 days out from the beginning of other shocks. That suggests that this one isn’t, in fact, completely out of the ballpark for this time period:

Source: "This Crisis is Not Different"

The "Iran II" incident refers to when the US oil majors reneged on long-term delivery contracts to Japan, sending Japan into the spot market bidding up prices accordingly. Verleger puts both the 30 and 60 day effects on a chart and notes that, if this supply shock - netting out at about 9% of crude now – continues for 60 days, then it may well look more like $170 - $200 oil.

LINKS

Gang of Coors: Trump and Mao in end times - Jeremy Wallace

The Missing Model: Why finance has no good framework for commodity procurement under geopolitical risk - Alex Turnbull

'Strange bedfellows' in American politics - Caravanserai

Add a comment: