Talking points for no-cost loans

I’ve been organizing with the Action Center on Race and the Economy and Lilac to demand no-cost loans for local governments from the Federal Reserve. (Sign up and come to the event! It’s today at 430pm EST.)

Since certified badass City Councilwoman Kendra Brooks is introducing a resolution supporting this demand, I thought I’d lay out some talking points to people who might not be convinced this is a good idea.

One pressure point is interest.

We’re demanding there shouldn’t be interest on these loans to local governments. No-cost loans. Local governments like school districts should only have to pay back the principal amount of the loan and nothing more.

But as the Philly Young Republicans reminded us in a snarky little tweet responding to Brooks, no-cost loans for local governments like school districts are a swipe against interest. We want ‘free money’, they might say.

What should we say in response?

Corporate bonds are low

First, interest rates are so low right now that a lot of capitalists are getting basically free loans. Just for an example, let’s look at the the High Quality Market Corporate Bond Spot Rate, or what one kind of ‘safe’ corporate bonds are yielding these days.

The 30-year rate hit its historic low of 2.79% in July 2020. But take a look at the 2-year rate at its historic low of .37%. Go back to before the pandemic it was above 2%. These are very low rates as you can see from the graph.

The low rates are generally part of the Federal Reserve’s bazooka approach to the economic crisis of the pandemic. Like the now broken-up Daft Punk said: harder, better, faster, stronger.

So corporations are getting really low rates for their loans. In some cases near zero. Why can’t local governments?

Zombies

Our Young Republican friends might respond: local governments are corrupt, inefficient, and don’t manage themselves well. Why should we help them out?

Well, I’d ask, if you’re so concerned about efficiency and good management, why do you let zombies thrive in our midst?!

Yes, I’m referring to zombie firms, which is a technical term referring to companies that don’t make enough profits to cover their annual debt payments.

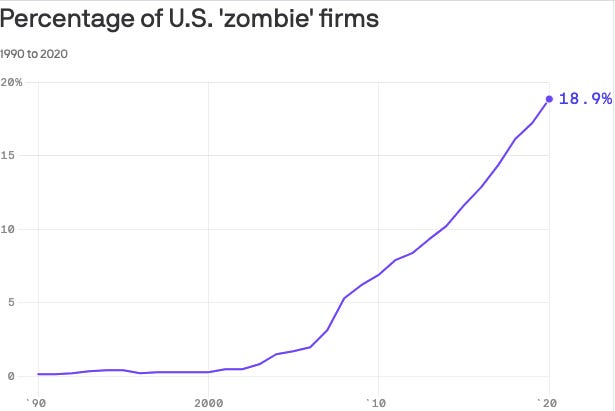

Axios reports that the number of zombie firms in the United States is nearing 20% as of 2020.

Sorry, I couldn’t resist a good zombie pic. The graph is just as scary:

A fifth of companies are walking around undead, unable to pay their debts. According to the sacred laws of capitalism these companies should go under. But do they? No. They keep getting loans.

Are there consequences for them, like there are for working class people who can’t pay their debts? No. They just keep on keeping on. We can’t let the ruling class fail by golly!

My point is that there’s a double standard when it comes to calling for low-cost loans to local governments. School districts and other public services vital to the working class get left out to dry while private firm after private firm turns zombie.

Inflation

I think we’ve dealt with the Young Republicans. The more advanced conservatives out there take another tack and bark about inflation. Sometimes they use the metaphor of ‘overheating’ to talk about this.

We can’t provide no-cost loans to local governments for the same reason we can’t be generous in our public spending: asset prices will go up. Inflation happens. Economy overheats.

Good ol’ Pat Toomey put Jerome Powell to the question on this issue earlier this week. And headline after headline says inflation is on the way.

This topic needs more study and I’m going to be following Nathan Tankus’s new focus on it in the coming weeks. But the consensus at least from from the new Monetary Optimists of the finance world—confirmed by the Fed’s new approach to unemployment—is that inflation just isn’t a thing like we thought it was.

Take a look at rental housing deflation, for instance, which fell below 2% for the first time since 2011.

Joe Wiesenthal is calling people concerned about government spending and inflation “truthers” given their brazen ignoring of facts.

This support for spending (a new monetary social democracy maybe?) must hold at the highest levels of the federal government if you look at the Biden administration’s American Rescue Plan.

So there’s good evidence that we don’t need to worry about inflation.

Reformist reform?

The last question I’ll pose is from the socialist. Are no-cost loans from the Fed just reformist reforms? Will they really undermine capitalism and move us towards cooperative relations of production?

Tim Barker’s essay yesterday on the anti-labor basis for the spending regime (which he calls the new corporate liberalism) asks a fair question: isn’t this lack of inflation fear underwritten by diminished working class bargaining power?

It’s important to note that Bureau of Labor Statistics came out showing that strikes decreased. Doug Henwood finds that Americans aren’t striking.

For sure, Barker says new spending “cannot be ruled out as forms that can accommodate large infusions of government money without threatening existing patterns of power and resources.” (And now I’m generally interested in the connection between inflation and wages.)

This, to me, is the best question: How do we tell a reformist reform in this post-neoliberal interregnum? Will these Fed loans weaken capital enough and empower the working class enough to move things?

Passing the PRO act will be a test of a ‘new regime’ in the way Barker says. But one thing I know is that the ruling class parks a lot of money in municipal bonds since their interest payments can be almost or completely tax-free. They’re tax havens in our own country.

At most, if we get no-cost loans then local governments won’t have to rely on these markets. We could push the ruling class out of these havens. Maybe they’ll have to make a move that weakens their position. At least, we can get rid of a Grima Wormtongue sitting at the side of local finance directors.

And maybe there’ll be fewer kids and teachers that get sick from toxic schools, which is the whole point.