Spreading thin

Corporate debt spreads, here I come.

This weekend I set myself the task of trying to understand this short piece at Econospeak on corporate credit spreads during the coronavirus crisis compared to the financial crisis in 2008.

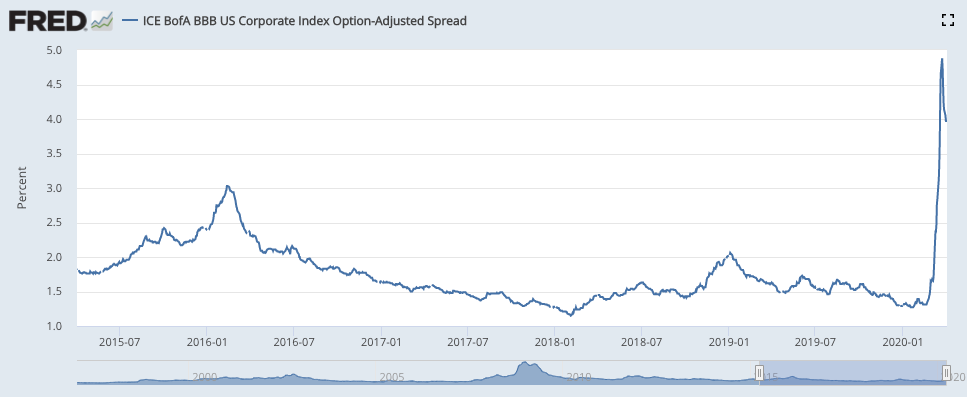

The article is saying that corporate credit spreads on high-rated corporate bonds shot up to 4% during the pandemic. Here’s one graph that shows the spike for Bank of America BBB credit.

In 2008, when Lehman Brothers collapsed, this spread was at 5%. So we’re not at 2008 levels of intensity here (and you can even see it coming down a little in this graph).

So what’s happening here? I think I have some beginning understanding of this idea of corporate debt spreads.

Willingness to Risk

Basically, that 4% number is the willingness that lenders have to lend money in this market. When spreads are low, lenders are willing. They’re giving loans at lower rates. If it’s higher, they’re being more apprehensive to give the loan.

But the spread itself is a relative interest rate for that market, compared to Treasuries (very safe) or higher-grade bonds (somewhat safe).

Let’s take two people, Borrower and Lender. Borrower is looking for a loan and Lender is considering whether or not they should lend people anything.

There are a lot of different markets for these loans. Borrowers and Lenders come and buy and sell them. It’s a way of getting and making money. People get money by borrowing and other people can get money by lending because the borrowers have to pay them back with interest.

The trick (as always) is how to make the most money. Here the lenders are calculating that. They decide what’s a good bet to make money off a loan using all kinds of measures.

There are safe and risky markets. The safest is a Treasury, or a government bond. Typically the 10-year Treasury bond is the benchmark, but there are others like corporate bond markets where people buy and sell credit in private companies.

One way to tell if a bond is a good bet is the bond ratings system, which is a lot like grades (or rather grades are a lot like the ratings system). There’s higher-grade bonds (safe bet) and lower-grade bonds (less safe). And then there’s ‘junk’ (risky).

For instance, the Philadelphia School District just got upgraded by Moody’s to Baa3. This is pretty exciting because that’s the line between low-grade and junk. The school district isn’t a junk bond, which means more Lenders will see it as a safer bet, lower rates, etc.

In any case, when the spreads between corporate bonds, and between corporate bonds and treasuries, are low more Lenders give to more Borrowers. But when they’re high, Lenders pause more, take second looks, and do more teeth-checking. The risk is higher, the returns less certain.

Why should socialists care about corporate credit spreads?

So I find myself wondering what socialists can make of corporate credit spreads once/if we get a more solid understanding. Here’s a few thoughts:

1) Such spreads are a good barometer of capitalist pain. If the spreads are high, then the capitalists are feeling it. If low, they’re running wild. This can have mixed consequences for labor.

On the one hand, if capital’s hurting, then firms will trim and cut to survive, which means making labor hurt through layoffs, pay reductions, benefit reductions, etc. One the other hand, if capital’s hurting, labor can take note and know that it’s a time to strike figuratively and metaphorically.

2) Spreads are all ruling class shit, but there’s stratification within the class. When spreads between high-grade, low-grade, and junk bonds get high then there’s more tension within the ruling class blocs active in this region of the mode of production.

3) Once again, spreads are an occasion here to imagine exactly what Socialist America will look like in terms of the mode of production. In a sense, finance basically means financing budgets. Production has costs. Where can/should the money come from to pay those costs in the short, long, and medium term in a socialist mode of production?

How would socialists finance budgets in a socialist mode of production? What would it mean for labor to control this process, rather than capital? Yugoslavia is one place to look for precedents. There could be lots of Chinese precedents to look at also.