Just Breathe?

The debate around reopening schools in the pandemic is about a lot of things: getting back to ‘normal’, having adults get back to work, not letting students fall behind, the struggle between teacher unions and districts, etc.

But one thing that’s getting more and more attention is ventilation. If your school doesn’t have good air flow, then it’ll be hard to open safely in the wake of a pandemic whose virus spreads in the air.

Ventilation is an infrastructure issue. It’s part of the school building. And school infrastructure is a blind spot in a blind spot in United States governance. People in charge across the spectrum, from capitalists to elected officials to district leaders, have let this problem fester.

The picture above is from Philadelphia, where the district has been installing plastic fans set into wood boards for ventilation, even though many of the district’s schools need millions of dollars of ventilation updates.

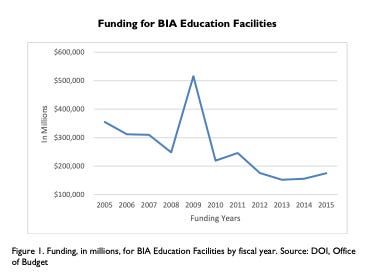

It’s a national problem. Some Inspector General numbers from 2016 are sobering. Funding for school infrastructure has been declining since 2005 (that spike most likely from TARP funds):

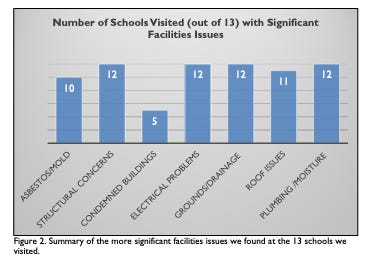

They visited 13 schools to randomly check on infrastructure needs. They found almost half of them condemned, and all but one of them had significant structural needs:

Democrats proposed a $100 billion school infrastructure plan in 2019. It didn’t go anywhere.

I don’t think anyone did this on purpose. I think it’s a structural issue: the way our system works is that many schools across urban and rural regions don’t get infrastructure updates, like ventilation.

The problem, like so many things with school, comes down to money. If you have financing you can do large-scale infrastructure projects. If you don’t, you can’t. So where does this money come from? Why is infrastructure so underfunded?

The wolves were already here

Jennifer Berkshire and Jack Schneider recently put out a book on a really important subject: school privatization. It’s called A Wolf at the Schoolhouse Door. (They also have a great podcast called Have You Heard that takes a progressive/critical look at education policy, history, and practice. Check it out.)

I’m looking forward to reading the entire book, but I’ve read a number of excerpts and it’s right about a lot of things: if we’re not careful, our public school system could become fully privatized.

One thing I haven’t seen in the excerpts (and might be in the main text), is that when it comes to school infrastructure—the schoolhouse itself—the wolves have already come and gone.

School infrastructure finance is a thoroughly privatized affair. Schneider is an historian, so he’s probably aware of the history of municipal bond markets and their integral part in providing loans for capital projects like ventilation.

It’s hard to get enough money fast enough for a public works project like school ventilation, so credit markets have traditionally been a way for school districts to get what they need. But historians are only now understanding how we got to where we are now.

Destin Jenkins’s work is really great on this question when it comes to city schools.

A seldom-told story is that municipal debt is the primary way cities fund infrastructure. In good times and bad, amid economic growth and budgetary shortfalls, cities regularly issue bonds to finance water and sewage systems, schools and parks.

It works like this. Cities issue bonds through the private bond market — a network of banks, investors, credit rating analysts and sellers of information who stake their fortunes on the infrastructural needs of everyday Americans. Just as Ford’s Detroit automobile plants gave rise to manufacturers supplying ancillary machinery and parts, the sale of a bond affords real estate developers, pipe manufacturers, concrete suppliers and glassmakers the opportunity to profit through the conversion of borrowed funds into basic infrastructure. In exchange for lending, bondholders collect principal and tax-exempt interest income backed by layers of guarantees. Although yields are relatively low, municipal debt is one of the safest assets and bondholders hold all the advantages.

The schoolhouse was always privatized. The wolves have been having their way for generations. And it’s only gotten worse in the last fifty years.

Michael Glass’s recent work on the history of pension-funded school infrastructure is illuminating, focusing on the suburbs as well. Yes, school infrastructure was financed through bond markets. But not all credit markets are equal.

There was an earlier period, tracking from around 1920 when public pensions became centralized, that comptrollers used something called fiscal mutualism where the wolves were put to a better use.

Public employees pay into their pensions every month. The comptrollers manage that money.

In fiscal mutualism, these comptrollers by law had to invest in municipal projects. They bought bond from local governments to finance infrastructure, including schools. There was a cycle of investment and support. Not perfect, of course, but it meant there was ample credit at low interest rates using public funds.

Fiscal mutualism came to an end in the late 1950s when returns on municipal bonds weren’t super high. Comptrollers wanted more bang for their buck. Laws forcing them to invest in public infrastructure were removed (‘liberalized’ they called it). They started investing in the private sector instead.

Cheap credit for public school infrastructure ended. Interest rates went up. And we’re still living in that world. Only now, people want schools to reopen safely—but they weren’t safe in the first place.

Hopefully the crisis kicks something into gear. I’d like to ask Michael Glass if some kind of better fiscal mutualism is a path forward: more laws about pensions funding public infrastructure could help. So could public banks, routine federal intervention, and policies that even out municipal revenues from wildly unequal real estate prices.