Getting swappy

File this one under Things You Probably Didn’t Know School Districts Do Under Capitalism.

It turns out two school districts in Pennsylvania lost millions of dollars betting on interest rates. They made a deal betting that the rates would go a certain direction (in this case up), but the rates have stayed so low that they now owe Wall Street money.

It’s called an interest rate swap. And yes, school districts do it.

Upper Merion owes $25 million. Colonial SD owes $8 million. Conestoga SD just passed a resolution to do the same on a $115 million bond. What’s going on here? Is this common?

WTF is an interest rate swap

Okay, so maybe you don’t understand what an interest rate swap is. The best I can do is tell you that it’s a “contract between two parties to exchange all future interest rate payments forthcoming from a bond or loan.”

There are different kinds of interest rate swaps. The most common is ‘vanilla’, where one party swaps the risk of an adjustable rate bond with a party whose bond is fixed.

This made me think of vanilla wafers. Not sure why. Just free associating. Maybe an interest rate swap is a vanilla waffler since it goes up and down with interest rates?

Let’s start over. When you buy a bond you’re lending to someone with the promise that you’ll make money when they pay you back. The amount of money you’ll get when they pay you back is determined by the interest rate, which is like the price of the loan. The interest rates go up and down.

Thus people can make money lending money. But, since interest rates go up and down, they can also make money betting on how much money people will make when lending money, depending on the changes.

I know I know, this is like eating cardboard. But it’s capitalism folks! If you want to imagine and different system you have to understand how the current one works. In another post, I likened swaps to the scene in You, Me, and Everyone We Know where the kids are talking about passing poop between butts forever and ever.

When you do an interest rate swap, you trade the risk of the loan getting pricier with someone else who’s willing to make money on the chance that it will or won’t. The interest rate swap is a kind of derivative, or a financial instrument that derives its value from a change happening in another financial thing.

It’s about lessening risk. If you can anticipate a change in interest rates, you can save your people money since—with a swap—you can prevent losing it if you make the right bet.

Nilla wafflers: does it work?

These swaps boomed in the go-go banking days of the 80s and 90s. Apparently, worldwide, there were about $3 billion of them in 1982. In 1993, it was $6 trillion. That’s a lot of swappy swap. Here’s some recent data on them in the US.

Local governments got into the game around the same time. There were laws against entities like school districts doing this, but these laws changed in the 90s. Looks like it became legal in Pennsylvania in 1996, when it was added to Title 53.

A study in 2009 found that, in six years, more than 100 school districts did swaps in PA. I haven’t been able to find recent data about school district interest rate swapping. Seems like districts do it a good amount.

Is this a good idea?

Certainly it’s a tool in the toolbox for reducing risk, and Redmond cites some success stories, but there are more recent arguments that, on the whole, local governments haven’t done that well using interest rate swaps.

Turns out go-go banking finance is about as reliable as a drunk driver. Whodathunk.

Bad news

Oakland lost a ton of money on a 1997 swap after the market went to shit in 2008. Who saw that one coming?

There’s an interest rate swap at the center of the Detroit water crisis, too. Bankers’ manipulation of the LIBOR rate led to the water authority’s bankruptcy, a study of racial capitalism in municipal finance.

The only accountant in the Pennsylvania legislature tried to ban them in 2009. Didn’t pass, obviously.

I agree this is a bad idea. The reason is that interest rates go up and down with the crisis cycles of capitalism itself, and people get it seriously wrong.

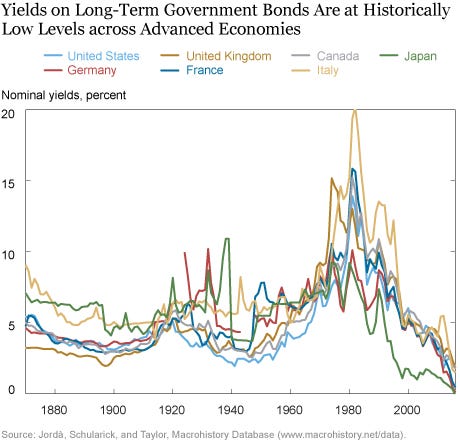

Trying to guess at patterns like this graph is difficult. Who thought there’d be a pandemic, for instance? Or any of the crises that took the economy by surprise? Do we think school district finance managers are capable of doing this? Should they even have the option?

No. They shouldn’t. We don’t need school districts doing go-go banking.

Hat tip to reader and comrade Jeremy L. for sending the original article my way.