DOE a Dear!

Well what do we have here?

Apparently President-Elect Biden saved himself a juicy morsel of funding at the Department of Energy when he oversaw the last global crisis as Vice President.

The morsel is about $40 billion in unused loan authority.

Could school districts take advantage of this? For example, Philadelphia’s school district needs about $4.5 billion in infrastructure improvements that no one in the city or state knows how to pay for. This includes asbestos remediation that’s killing teachers and way out of date ventilation system that will be key for reopening as the we fight the pandemic. A green approach to this problem could save schools, lives, and livelihoods in Philly.

Could Philly or other school districts get ahold of a loan from the DOE for green school infrastructure improvements? Let’s see.

Innovative Energy

The DOE has three programs that issues loans: one for tribal energy programs, one for vehicles, and the last for “innovative energy” initiatives called the Title XVIII program:

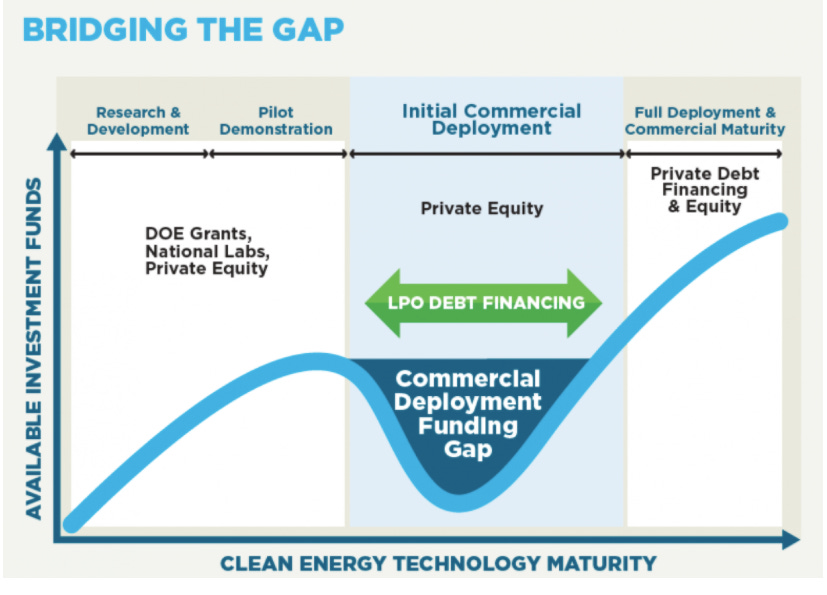

The Title XVII Innovative Energy Loan Guarantee Program is LPO’s largest and longest-standing program, providing more than $25 billion in loan guarantees to 25 energy projects since 2007. Title XVII was designed to help energy project developers bridge the technological “valley of death,” a key point in the innovation lifecycle when new projects possess the highest risk of failure, making private investment difficult to attract.

In a graph with friendly colors, the idea here is to bridge the gap between green projects and investment. This is very promising.

The portfolio of loans guaranteed spans the country, including both green companies in the private sector and public entities. One interesting precedent is a nuclear energy initiative with the George Power Company and the Municipal Electric Company of Georgia.

The DOE’s website for the program has a generous set of eligibility criteria:

Utilize a new or significantly improved technology;

Avoid, reduce or sequester greenhouse gases;

Be located in the United States; and,

Have a reasonable prospect of repayment.

Could a school district apply? Let’s dig into these. I’m particularly interested in the kind of entities they’re imagining and what ‘reasonable project of repayment’ really means.

Details

This is a loan guarantee program, which means that a borrower takes out a loan that’s backed by the Department of Energy. If the borrower defaults, the guarantor assumes a certain amount of the debt.

The piece of relevant legislation is the Energy Policy Act of 2005, and the Final Rule (10 CFR 609, dated October 23, 2007, as amended on December 4, 2009, May 21, 2012, and January 17, 2017) that provides guidance. We’re interested in how the funding works. It looks like the generosity continues. The legislation and guidance

authorizes the Secretary, after consultation with the Secretary of the Treasury, to enter into loan guarantees on such terms and conditions as he or she determines to be appropriate, in accordance with the provisions of section 1702. Section 1702 also directs the Secretary to include in loan guarantees “such detailed terms and conditions as the Secretary determines appropriate to (i) protect the interests of the United States in the case of a default; and (ii) have available all the patents and technology necessary for any person selected, including the Secretary, to complete and operate the project.” (42 U.S.C. 16512(g)(2)(c)).

Maybe they’re hiding some dirty terms and conditions in 1702. But they’re not! I’m used to rightwing perverts at the Fed, and comparatively speaking these are great conditions. Check out the language around interest rate and term of the loan:

(e) Interest rate

An obligation shall bear interest at a rate that does not exceed a level that the Secretary determines appropriate, taking into account the prevailing rate of interest in the private sector for similar loans and risks.

(f) Term

The term of an obligation shall require full repayment over a period not to exceed the lesser of—

(1) 30 years; or

(2) 90 percent of the projected useful life of the physical asset to be financed by the obligation (as determined by the Secretary).

A lot is up to the secretary’s discretion. And 30 years is great. It’s like a mortgage! (There’s an IRS question for school districts, we should note: I read recently that a district can only hold onto issuance revenue for 30 months. Need to look into that more, though if the district enters into an agreement with a green company then maybe the issuance goes to the company?)

The only line that bugs me is that they want to take into account “the prevailing rate of interest in the private sector for similar loans and risks.”

I’m not sure if there’s an ‘and’ or an ‘or’ there, exactly. Would the Secretary just defer to the municipal bond market for rates, let Wells Fargo or whoever underwrite it with a high interest rate, and the district gets hosed?

There’s some more info on the FAQ sheet:

The interest rate for loans that are issued by the Federal Financing Bank (FFB) and backed by a 100 percent DOE loan guarantee will be calculated at the applicable U.S. Treasury rate for the tenor of the loan plus a FFB liquidity spread and a risk-based charge that may be collected up front or as a credit-based interest rate spread over the life of the loan. Learn more about the credit-based interest rate spread for Title 17.

Oh, and also: if you’re not doing a vehicle project, you might have to pay $400,000 in application fees.

This about the debt to equity ratio also seems relevant:

The average debt-to-equity ratio for an LPO project is 65 to 35 percent. That is, loan applicants invest 35 percent private capital into a project and cover the remaining through public debt financing.

Process

How does one go about getting such a loan, and who has in the past?

Under the Title XVIII innovative energy program in the LPO, there are several loan guarantee subgroups. The relevant one for such a project as the school district would probably be the Renewable Energy and Efficient Energy Projects loan guarantees.

With a smile on my face, I click on the helpful FAQ sheet and get the answers I’m looking for. (I lose the smile a bit when I see that the program “has up to $4.5 billion in loan guarantee” and I’m not sure if that means total or per loan. The Georgia deal got up to $5.1 billion, though, so who knows.)

Would you look at that: the FAQ sheet says that the LPO can finance

Efficiency Improvements Improve or reduce energy usage in residential, institutional, and commercial facilities, buildings, and/or processes; and recover, store, or dispatch waste energy or underused renewable energy sources

They say they offer

access to capital, flexible financing, and expert project support to help reinvigorate, advance, and transform America’s energy infrastructure.

They make the loan application process sound almost fun:

Pre-Application Consultation: Engage with LPO for a no-fee, pre-application consultation to review project technology areas and basic eligibility requirements.

Formal Application Process: Submit Part I application to LPO to determine basic eligibility, followed by a more thorough Part II application to determine project viability.

Due Diligence & Term Sheet Negotiation: Enter due diligence, negotiate term sheet, and receive a conditional commitment offer.

Loan Closing & Project Monitoring: Negotiate and execute loan documents. After loan closing, LPO monitors construction and operation throughout the life of the loan

So all we have to do is contact the LPO to schedule a no-fee, pre-application consultation at LGProgram@hq.doe.gov. Question is, who should this be? Partnership between companies and governments? Just companies? Something to think about.

The loan solicitation document is a beast and I’ll need to take some time with it. But just from the title material I see the loan guarantees are through March 2022, so there’s time.

Going to look into this more! Stay tuned.