Data confusion

Once again I have to recommend Econoday Unplugged for straight talk when it comes to the economy. It’s just a soft-spoken American guy who stutters a bit and an oddly charismatic British guy going over numbers.

Yesterday’s episode had a helpful segment (start at 4:80) on just how confusing data is given the lock downs, particularly leading indicators:

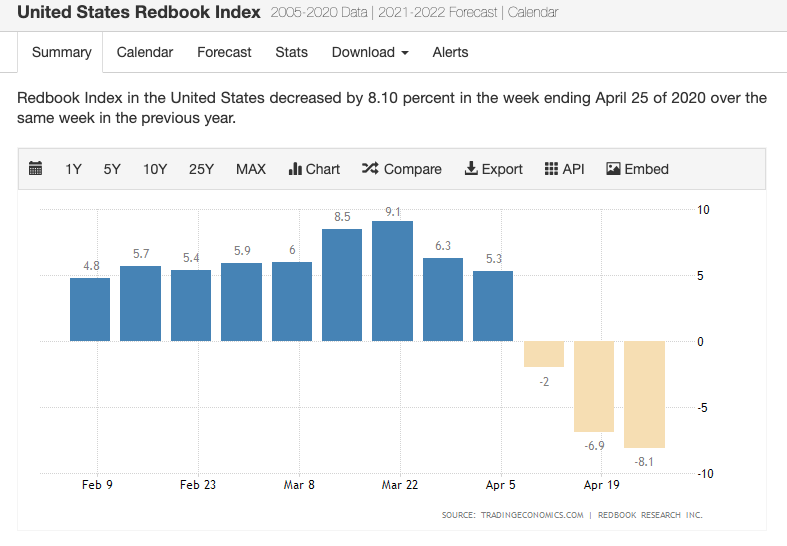

We had Redbook today [pictured above], weekly chain-store/same store indicator, which tracks essentials in consumer goods. It peaked out out double digit growth as people stocked up but now it’s coming down in double digits.

There’s going to be so many dislocations in the data. We had inventories today, and retail inventories shot up higher than March because of the close down of car dealers. That made for a big huge build that’s going to offset a big huge draw at the wholesale level. The numbers are going to be hard to figure out. There’s going to be odd cross-currents.

Like these PMIs and composite indexes, I want to personally say: delivery times don’t belong in the composite index during a crisis. When you go back and look at these composites they’re not going to make sense. They’re actually stable here in the US because of the gigantic spike in delivery times, which isn’t a positive at all. That’s an example of the kind of data confusion we’re going to be getting.

I look at these numbers to try and understand what’s happening in production and yeah, it’s true. What do they mean right now? How are they calculated? Why include delivery times in the manufacturing index in the first place, and then how can we take that seriously given the distortion of the lockdown? And how many measures like that are there?

Looking at the Institute for Supply Management’s index (which Alan Greenspan said was the one number you should look at in an economy), tracking changes in supply and purchasing orders we see huge decreases.

The ISM Non-Manufacturing PMI for the US fell to 52.5 in March of 2020 from 57.3 in the previous month and beating market forecasts of 44. Still, the figures pointed to the weakest expansion in the services sector since August of 2016 and the largest monthly drop in the headline PMI since September of 1997 mainly due to supply problems related to the coronavirus. Declines were seen for business activity (48 from 57.8), employment (47 from 55.6), inventories (41.5 from 53.9) and new export orders (45.9 from 55.6) while new orders (52.9 from 63.1) and supplier deliveries (62.1 from 52.4) grew less.

Meanwhile of course the stock market kinda rallies off and on, based on information as it comes in.

Of course the ideology that articulates the fluctuations are the DOW with the ‘economy’ is very misguided. But even when you look at the numbers in production itself, there’s going to be confusion.

Generally, I think socialists should dig into these numbers, try to get a picture of the dominant mode of production to understand production itself. I find myself wondering what the measurements and composites and indexes would look like from labor-facing, socialist economists.