Chinese municipal bonds

I've been curious about Chinese municipal bonds because the country has been characterized as a kind of challenger to the western hegemony in the world: we're always in competition with China, becoming more aggressive towards them, even though we've relied on their manufacturing base for decades and built them up. Anyway, I'm interested in if/how China does it, and here we have researchers who have recently looked at the issue.

Recent research tells the history of the Chinese municipal bond market, how it's regulated, and then the authors measure the price of something called an "implicit guarantee," unique to that market.

They talk about something called "hidden debt," specifically how it's been regulated by the national government, finding that the regulations make it harder for municipalities that can't give an implicit guarantee. It's more expensive for these places with lower fiscal capacity to borrow and then get revenue for infrastructure.

Basically, we're looking at this so we can get a sense of how China does it and then think about how we do it differently. So I’ll go through a timeline of policies, the important takeaways, and finally a compare/contrast with the US municipal bond regime.

1. Timeline and definitions

1994: The Budget Law is passed, a tax sharing reform, which "aimed to redistribute central and local taxes" and ultimately reduced local revenue while increasing the pressure to spend locally. Municipalities created local government financing vehicles to take out loans to fill the gap (LGFV). They weren't allowed to issue bonds but they did anyway, basically.

Budget constraints were interpreted as "soft," meaning that they could be bent. The LGFVs became a kind of 'state owned enterprise' which come with varying degrees of confidence that the municipality could pay the loan with interest--it wasn't the municipality wink wink. This is why their debt is hidden and the guarantees are implicit.

Thus the "implicit guarantee" formed: the LGFV would guarantee repayment based on their revenues. This 'implicit guarantee' is basically just a market signal, very similar to what we have in the US, except in China it's unstated because municipalities aren't allowed to borrow like this.

This created what they call the "price of an implicit guarantee," which they define as "the extent of the IG estimated by the market can be measured by the spread of LGFV bonds: a narrower spread suggests a higher level of expectation for implicit guarantee." A spread is just the difference between yields on bonds: a bond that comes with a high yield vs. low yield. So, again, implicit guarantee is just the price of the bond in this more furtive sense. I'm not sure I fully understand this, maybe others do.

2008: In the wake of the financial crisis, the economy was recovering, and regulations on LGFV were loose. The central government encouraged all kinds of borrowing to increase revenues for localities in the recovery.

2010 - 2014: In the froth, some standards and regulations were put in place.

2014: The first strict regulations on LGFV in "The Revision of the Budget Law and the Opinions of the State Council on Strengthening the Management of Local Debt. The goal was to lower risk for localities when it came to debt. Although apparently enforcement was lax. This was called Document 43.

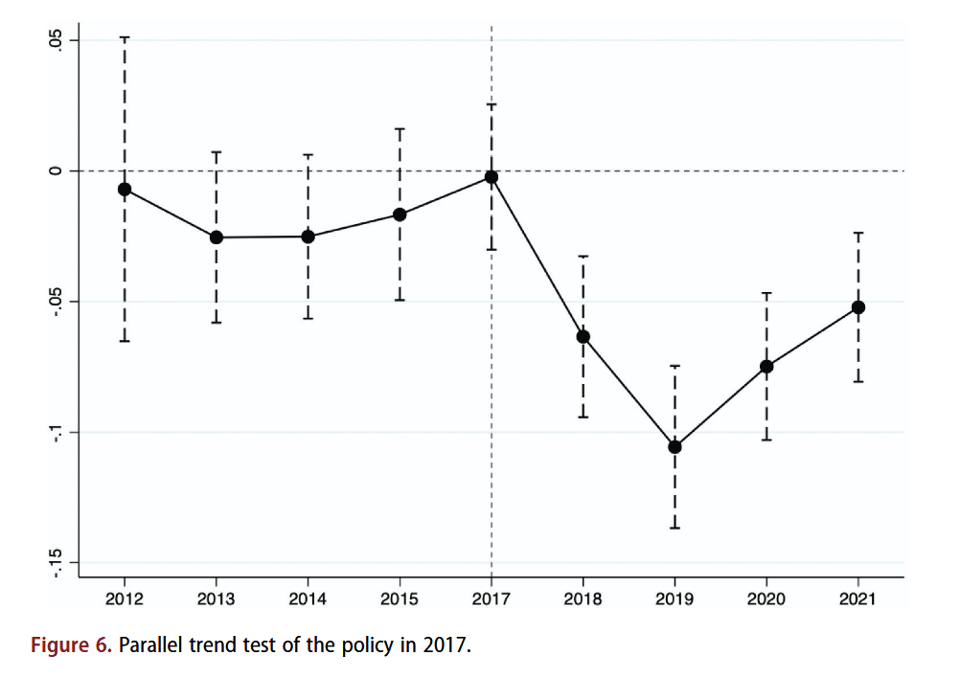

2017: Another measure was put in place to enforce the regulations, "The Notice on Further Regulating the Debt Raising and Financing Practices of Local Governments." This involved monitoring and joint supervision of local debt, encourage better management and control. But all of this decreased bond issuance. The soft constraint became hard. The National Financial Work Conference took a hard position on this. This is the year of the policy shock.

2018: Development and Reform Commission in Document No 194 required the separation of governments from LGFVs. Also in this year, the Ministry of Finance published Document No 23 that regulated state-owned enterprises more to prohibit them being involved with local financing.

2. Question and methods

The researchers want to know whether it's in fact true that stronger fiscal capacity of the municipality decreases the price of the implicit guarantee. They measure fiscal capacity through external guarantees. During this period of increase regulation.

They got their data from the Shanghai Stock Exchange, Shenzen Stock Exchange, and Interback Dealers Association, bonds between 2012-2021. They also get data from the Wind Database and the Guangfa Fixed income Database. 10,619 LGFV bonds total.

They guess that more implicit guarantee lowers the spread, that central regulation weakens implicit guarantees, and those central regulations impact localities with weaker fiscal strength.

3. Findings

Average spread increases as the local government moves upwards, from province to municipality to county. They find that "the greater the degree of implicit guarantee, the lower the spread of LGFV on issuance of LGFV bonds.

In figure 4, they show that lower-rated bonds have a consistently higher spread, confirming their sense that there's a higher price for weaker implicit guarantee. Issuance spreads increased after 2017.

When they track the spreads over time, they stay still in 2014 moving forward (probably with the lack of enforcement), until 2017 then up again in 2019 when things got strict in the wake of the 2018 regulation. That movement of the spreads comes from the regulatory shock.

They're trying to "open the right door" in the process of "blocking the wrong door." How do you get someone to go through a door? One way is to open that door for them. The other is to block every other door they could go through.

The story here is about the central government getting involved in local borrowing. The smaller the locality, the more their 'meddling' impacts the price of their lending, and government meddling happened in earnest after 2017.

4. Reflection - compare/contrast

There are similarities and differences between the Chinese and US bond markets that I can decipher.

Differences

(i) Chinese bond market is much much younger and, I imagine, smaller than the US.

(ii) the Chinese central government has taken much more active role in limiting local debt, first performatively and then robustly.

(iii) China has state owned enterprises, which are connected to the government in much more intentional ways through central planning. While it has a decentralized economy, it's political system is centralized.

(iv) There's a sneaky dialectic of restriction and circumvention that falls along implicit and explicit lines. While the central government messages that it wants to redistribute and create equality, it permits localities to borrow, and they do so under the guise of state owned enterprises who borrow on behalf of the locality. There are soft budget constraints, implicit guarantees, and hidden debt.

(v) That sneaky dynamic ran headlong into an actively regulating central government that cracked down on local debt and didn't hesitate to throw local debt markets into 'disarray' to try and regulate the situation, we can see this from the reforms of 2017 onward.

Similarities

(i) There are, in fact, municipal bond markets in each country. Each country permits localities to borrow, but that permissions takes different forms. In the US, we have tax exemption of municipal bond interest. In China, you can't really do this borrowing, but there are SOEs whose purpose is to borrow for the locality, which is a sort of permission.

(ii) These municipal bond markets operate in a dialectic of restriction and circumvention of some kind. The US does this too.

(iii) The restrictions on local borrowing happen for both political and fiscal reasons. The US regulates local borrowing too: but it's states that put in debt limits, bond referenda, and then the federal government only limits the amount which big banks can participate. It also regulates the compliance standards through the IRS (arbitrage rules, eg).

(iv) The authors confirm a dynamic that happens in the US: when a locality has a strong fiscal position, its borrowing costs decrease. In the US, this happens through credit ratings, interest rates, yields, coupons, etc., and the market of municipal bonds. In China, it happens through central government regulation, clamping down on explicit forms of lending.

(v) Smaller governments hurt as a result of the system.