An MLF Loan for a School District: The Details

On Monday I laid out a policy proposal for school funding in the covid crisis. School districts, urban and rural, should apply to the MLF for loans. In Philadelphia, the loan would go towards fixing ventilation systems and other infrastructure.

I got a lot of great feedback on that piece. In this essay I want to get to details and crunch some numbers.

But before that, I want to be clear that I’m not the first one to think of this proposal nor am I the only one working on it. I organize in a movement ecology of fantastic activists from whose knowledge and labor I benefit.

There are lots of organizers, scholars, and education people researching, unpacking, and pushing for this idea.

The Working Educators caucus of the Philadelphia Teachers’ Union spent years organizing on the toxic schools issue. The Debt Collective has been organizing around municipal and state debt viz. education for almost a decade and I have benefitted from conversations with organizers like Jason Wozniak, Tom Sgouros and others looking at these issues.

Coalitions like Our City Our Schools, the Alliance for a Just Philadelphia, and research organizations like ACRE are looking at federal loans to address school funding in equality. The #DemandSafeSchools movement in Philadelphia have been talking about using the Federal Reserve in this moment as well.

I’ve benefited from conversations with Scott Ferguson working with the Modern Money Network, and the team behind Money on the Left in thinking about this, particularly their proposals with economist Benjamin Wilson for higher education funding through a sovereign currency model called the Uni.

There are others I’m forgetting and will make sure to lift them up as I go along.

With that said, in this post, I want to look at some of the details in this proposal. What are the actual numbers going to look like? We’ve got to be clear-eyed going into this.

My case study will be the Philadelphia School District. Please someone tell me if I’m making a mistake!

The Amount

The first question is: how much are we going to ask for? Once we have that number we can start figuring out how much it’s going to cost to take out this loan.

In an earlier post I was angry and said we should ask for $6 billion. Unfortunately for my past self, that’s impossible.

Remember that the MLF loans can be up to 20% of gross revenues. The School District of Philadelphia brings in money from a General Fund, an Intermediate Unit Fund, and Categorical Funds. These revenues come in the form local taxes, state grants and subsidies, and federal grants and subsidies.

Here’s what the District brought in last year according to last year’s financial report (which has a cool picture of an astronaut on the cover, by the way—see above):

The total from the three funds is $3,634,320,991. Twenty percent of that total revenue is $725,864,198.20.

So we can ask for about $726 million dollars. What can we do with that money when it comes to ventilation updates across the district?

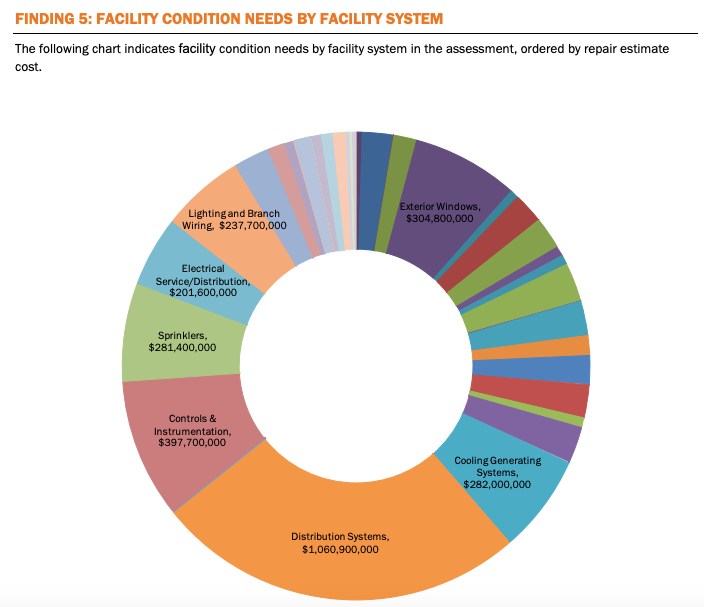

I have proposed that we get enough money to replace the ventilation systems. Do the numbers work? Luckily, the 2017 report on Philly’ schools’ infrastructure has breakdowns for type of improvements needed in city schools.

To me, the leading candidates would be things having to do with air circulation, HVAC, and health/safety measures.

The report does mention HVAC, but doesn’t use it as a category for pricing. The closest thing I’ve found is in “Finding 5,” where the report shows the cost of repairs by facility system like lighting, windows, and sprinklers.

Exterior windows and cooling generating systems together will cost about $587 million. That leaves $139 million breathing room for other costs (pun intended).

Given that this is a political project, I say we ask for the full $726 million. What do we have to lose?

Well, maybe something. Because there are the payments to service the loans as well as the origination fee.

The Interest

Remember that the Fed is offering to buy bonds here. That basically means giving the District money on the condition that the District will pay that money back according to certain terms and conditions. One of those is the interest rate.

In my previous post, I mentioned the interest rate of MLF loans, or the price of the loan. When you lend money there’s got to be something in it for the lender. The borrowers get the money, the lender gets the interest.

The Fed set out interest rates according to spreads, or rates relative to the Fed’s 10 year Treasury note. These spreads increase depending on credit rating and are measured in basis points, a fancy way of saying 1/100th or .001.

This means that the School District of Philadelphia would have a 3.8% rate on the loan. This is because the SDP has a Baa3 credit rating (which is part of what I call school finance’s cycle of bondage, more on that in future posts).

Its credit rating is a measure of its ability to pay the principal and interest of the loan. Its ability to pay back the loan is determined by its financial reliability, how much is coming in and whether it can service its debts. It’s all racial capitalism and forms the terrain of this proposal.

There’s an awful term in credit ratings. Under a certain grade of creditworthiness, an institution’s bonds are ‘junk’. Until 2019, the SDP’s loans were junk. Then it got a bump based on an increase in property values.

We need to figure out how much SDP would be paying on this loan. That’s 3.8% of the total amount of the loan, which is $27,582,839.53. (On top of paying back the principal.)

Not only is this steep, but it’s structurally racist. The School District of Philadelphia serves a majority minority population. It’s been subject to the combined pressures of deindustrialization, white flight, shrinking property values, and the deficit myth.

As I’ll detail in future posts, this information is part of the case for contesting the terms of the loan if and when the time comes.

Since, according to the MLF, a municipal government can only borrow the funds for up to three years, the support is not indefinite and there’s not a lot of between getting the money and being on the hook for it. Not only that, but the District will have to specify how it’ll going to pay the loan back.

The Origination Fee

Not only is there interest to pay, but there’s an origination fee that goes to the Fed. An origination fee is collected when getting a new account at a bank or other institution handling loans. Again, from the MLF website:

Each Eligible Issuer that participates in the Facility must pay an origination fee equal to 10 basis points of the principal amount of the Eligible Issuer’s notes purchased by the SPV. The origination fee may be paid from the proceeds of the issuance.

Remember that basis point are 1/100, or .001 of the amount you’re talking about. In this case, the Fed asks for a hundredth of the principal of the loan, or $725,864.19.

On the Hook?

According to the terms and conditions of MLF loans, the School District of Philadelphia would, on top paying back the original loan principal of $725,864,198.20, owe:

$725,864.19 (origination fee)

$27,582,839.53 (interest)

That’s $754,172,901.93. On a three year timeline. While that sounds like a big number, wait until you hear about the context.

As it stands, the district spends 9% of its FY2019-20 budget on existing debt service. They report a $3.4 billion expenditure budget. That means they pay $306 million just for one year’s debt service.

Once it got bumped up to non-junk, the district just recently issued $481,080,000 of bonds to private bondholders, packaged by big private banks like Bank of America and Morgan Stanley and CitiGroup.

I offer those numbers because the District is accustomed to making these sorts of deals. Like any of the other bonds it issued, of course there are risks for being on the hook for $726 million. The district’s credit rating is on the line. Which means it’s creditworthiness is on the line.

But this time it’s different.

Remember that the Fed is not like these lenders. It’s not a market actor. It’s Atlas holding up the market on its shoulders. It’s making an extraordinary offer. The terms and conditions it’s offering are more political than anything.

The Federal Reserve is a different kind of entity about which we should think differently. This loan is a political act. For instance, progressives in Congress are urging the Fed to reduce the MLF rate down to near zero. This is a fight we can take to them if we can organize.

I’ll be writing about this strategy in my next post. In general though, extreme times call for extreme moves and liquidity support to fund Philly schools’ ventilation systems should be that kind of move.