Peak Oil Part 2 — Iran War Edition

Energy Security Takes Center Stage

On a normal day, about 20 million barrels of crude oil and oil product moves through the Strait of Hormuz — nearly 20% of global oil supply. That trade has ground to a halt, as Iran has targeted tankers moving through the strait and oil infrastructure in nearby countries in retaliation for the American and Israeli bombing campaign. When the war started, oil futures were in the high $60s. As of this writing, prices are hovering around $100 per barrel.

In my last post, I talked about the role of U.S. shale oil in propping up oil production and what it means if that boom is coming to an end. The war has only made that question more urgent.

There are many unknowns about how things will unfold, especially in the short and medium term. Even if the war ends tomorrow, the world is facing serious economic pain. Countries that are net importers of energy will suffer shortages. The longer the war continues, the worse the pain will get.

Looking further out, however, the picture seems clearer. The 2026 Iran war is the second massive disruption of global energy markets in the last five years. Countries like China, which have already committed to reducing dependence on imported energy, will double down on energy independence through electrification and renewables. Other countries that are not as far along will more than likely pivot as well.

That doesn’t mean the transition to a renewable energy system will be easy. But it does seem increasingly inevitable.

A Historic Shock

To address the sudden loss of 20 percent of the world’s oil, IEA member nations, the U.S. and other countries opened the taps of their strategic oil reserves. But even with 300-400 million barrels available, analysts say the releases can only cover a fraction of supply. As Goldman Sachs commodity analyst Samantha Dart explained on Bloomberg Television.

The fastest release we’ve ever seen from the group was at a pace of about 2 to 2.5 million barrels per day. So on net, we are still likely to be losing over 10 million barrels a day of oil from the market.

Dart pointed out that there’s a difference between shutting in production and stopping exports. Stockpiling oil is one thing. Stopping production because there’s nowhere to put the oil is a bigger deal, which takes a lot longer to restart.

Unlike national oil companies like Saudi Aramco, the international oil companies (IOCs) do not typically hold spare production capacity in reserve. With Saudi excess capacity trapped behind the Strait of Hormuz, there’s no easy way to just open the taps to meet a sudden shortfall. (The Trump administration has, however, eased sanctions on Russia and is letting Iran itself sell more oil).

No worries: the U.S. is an oil exporter, right?

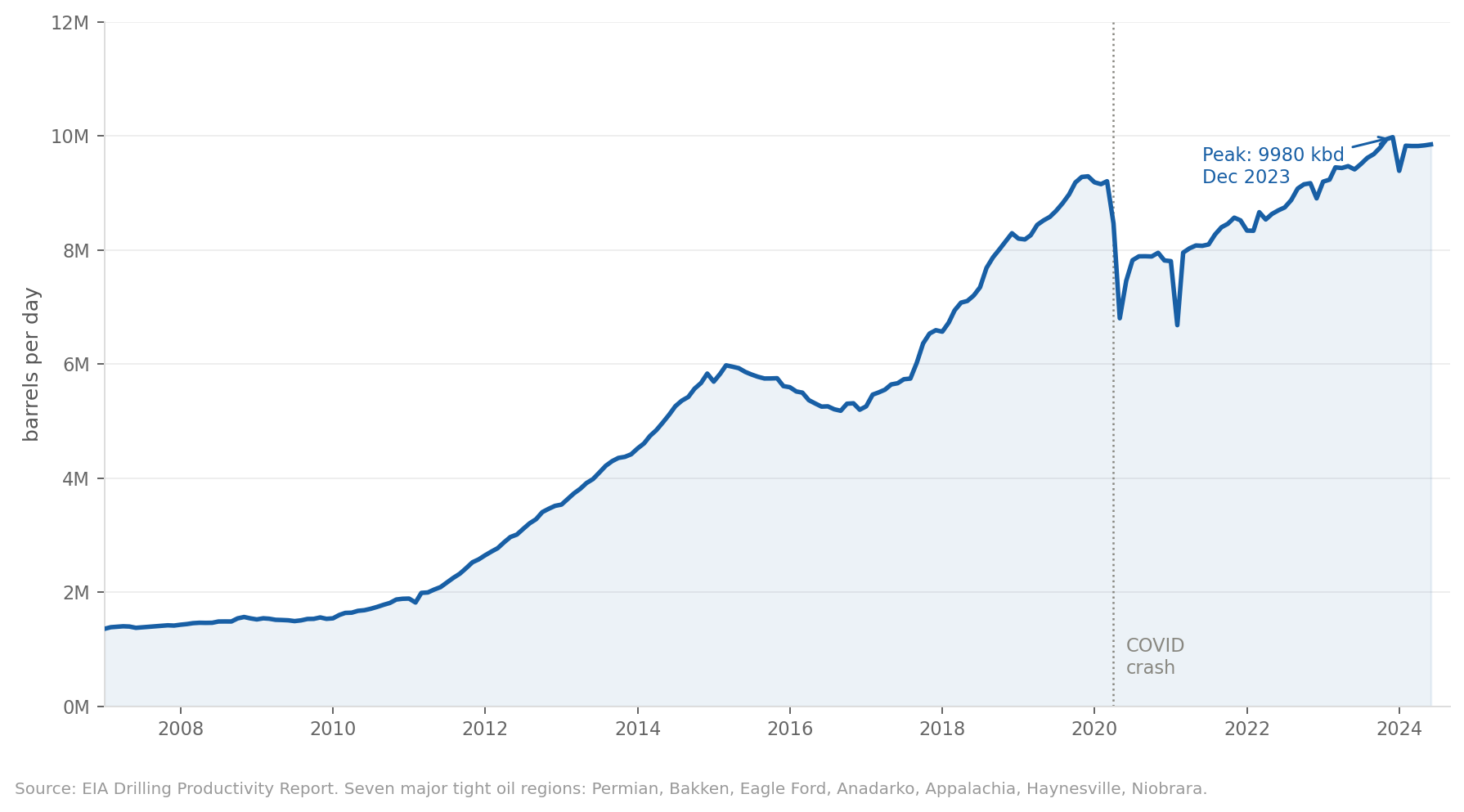

A big difference between this oil shock and previous disruptions in the 1970s and early 2000s is that the United States today produces much more oil than it did then. Starting around 2010, the fracking revolution opened up huge new reserves in shale deposits, making the U.S. the largest producer of oil in the world.

Energy secretary Chris Wright has pointed to our status as a net exporter to downplay the significance of energy disruptions from the war for Americans.

Put aside for now Wright’s implication that the economic pain and political repercussions of the war on Europe and Asia are unimportant. The fact that oil prices are set on the global market means that oil shocks hit the American consumer just like anyone else.

A more nuanced argument is that because of its production status, the U.S. economy as a whole is somewhat hedged against high oil prices. When prices go up, U.S. producers reap windfall revenues that theoretically trickle through the economy and offset the economic pain of high prices for consumers — though bigger dividends for oil producers is probably cold comfort for the average American consumer paying $5/gallon gas.

Won’t higher prices spur more oil production?

High oil prices in the mid-2000s kicked off the fracking revolution by making previously uneconomic reserves pencil out. In theory, that same dynamic would apply now, especially if prices go much higher and persist.

That’s not the message industry analysts are sending, however. As I discussed in my last post, in recent years, the early frenzy of drilling in the shale patch has given way to mergers, consolidation, and stock buybacks. This “capital discipline” generated huge cash flow, made the industry profitable, and allowed producers to pay down debt.

At least for the moment, analysts don’t see that strategy changing anytime soon. According to a report from the British market intelligence company Argus Media, shale producers have been “wedded to a policy of capital discipline for so long now that it would require a sea change in boardroom strategy to reverse course.” Instead, windfall profits will flow back to shareholders through stock buybacks and higher dividends.

The problem is that “maintenance mode” won’t be enough to even keep up current production, much less increase to address shortfalls. According to the EIA, U.S. crude production is set to fall next year.

Of course, the industry would like to present the story as one of “discipline” rather than geologic constraints. However you frame it, though, the truth is that major shale plays like the Bakken Formation and Eagle Ford Shale have already plateaued or declined in recent years, and even in the Permian, growth is anemic. Operators have exhausted their best drilling locations, and it seems unlikely they’ll be able to increase production from this point forward, no matter how expensive oil gets.

Let’s Talk About Natural Gas

As bad as the war is for oil, the implications for global natural gas markets are worse — with the outlook getting even darker in recent days.

As soon as the war started, the Gulf state Qatar was forced to shut down its liquefied natural gas (LNG) production, taking nearly 20% of the world’s supply off the market overnight. Recent forecasts of an LNG supply glut quickly gave way to concern that suppliers wouldn’t be able to meet demand.

On Wednesday, March 18th, Israel struck South Pars — the Iranian-controlled part of one of the largest natural gas fields in the world, and the largest source of Iran’s domestic energy supply. In response, Iran struck Ras Laffan Industrial City, doing significant damage to Qatar’s main LNG processing hub. According to Saad al-Kaabi, chief executive of QatarEnergy, a significant portion of Qatari gas will be offline for three to five years — what analysts call an “Armageddon scenario” for gas markets.

The news that much of the world’s LNG was now off the market caused European gas prices to spike by 35%. Many analysts believe the impact will be larger than Russia’s 2022 invasion of Ukraine.

Gas Made in America?

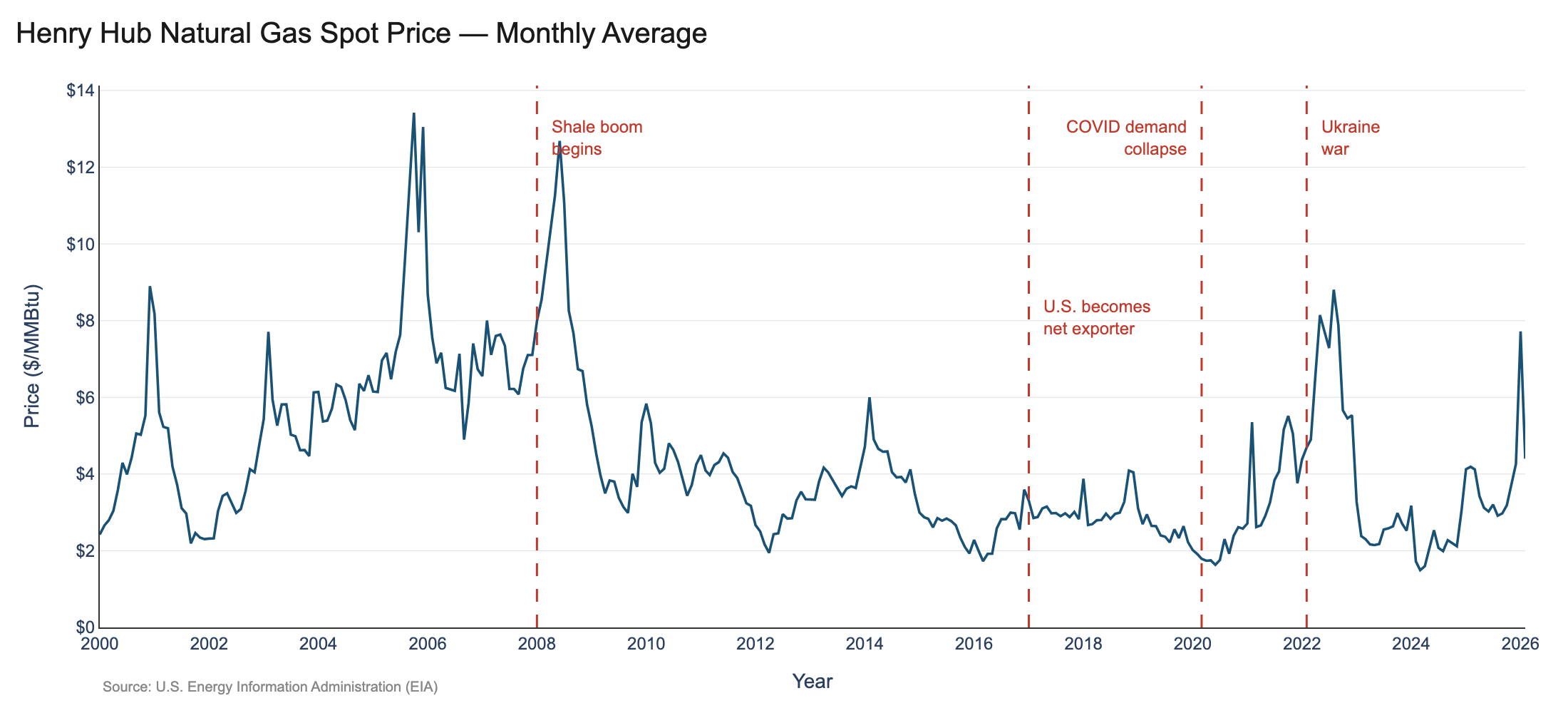

In addition to crude oil, the 2010s shale drilling boom in the U.S. unlocked vast new reserves of natural gas — so much gas that the United States started liquefying huge amounts of it to send overseas. The U.S. became a net exporter in 2017.

This shift had a number of implications.

In the past, natural gas markets were largely constrained by the reach pipelines. This meant that the vast majority of natural gas was produced, traded, bought, and sold domestically or across land borders to Canada or Mexico. With the growth of LNG, the U.S. natural gas market was, for the first time, exposed to global seaborne markets in Europe and Asia. When Russia invaded Ukraine in 2022 and European gas supplies were threatened, U.S. gas prices spiked.

However, natural gas markets are still more fragmented than oil. At the moment, U.S. LNG export terminals are at capacity, which means that domestic natural gas prices are still driven more by domestic supply and demand than the global supply crunch, according to OilPrice.com.

As with oil, there’s no immediate indication that gas drillers are planning to significantly increase production in response to the supply shock. The EIA forecasts almost flat production until 2050.

That level of growth is hard to square with some demand forecasts. According to a January 2026 Wood Mackenzie report:

The massive build-out of US LNG is expected to boost global supply faster than demand growth, resulting in European traded gas prices almost halving by 2030, when prices will be at their lowest levels, compared with 2025 … At the same time, growth in LNG supply and data centres in the US will boost local gas demand by almost 40% in the next 10 years, lifting domestic Henry Hub prices to an average US$4.9/mmbtu (€15/MWh) in the 2030-2035 period - 50% higher than the average price in 2025.

It’s worth noting that even if this analysis were correct and it were possible to boost U.S. gas production by 40%, it would likely still be bad news for American consumers, who would find themselves competing with European industry and domestic data centers to heat and power their homes.

But is 40% kind of growth even possible? Energy reporter Justin Mikulka, for one, is skeptical:

40% increase in U.S. gas demand? That is insane. Why? Because, as I’ve explained before … that amount of gas isn’t available from U.S. production. So, that ain’t happening … Henry Hub prices will be well over $5 with a 40% increase in demand. They will be higher than $5 at a much lower increase in demand, which is the only increase that is possible due to geological constraints - the gas isn’t there.

Windfall and Destruction

U.S. LNG exporters stand to make a killing on what they do export — at least in the short term. But as Ira Joseph, a senior research associate at Columbia University’s Center on Global Energy Policy, told Natural Gas Intelligence, sustained high prices could push Asian buyers out of the market permanently.

As recent article in Gas Outlook put it:

Gas executives have consistently promoted LNG as advantageous on three criteria – reliable, affordable, and clean. The last two of those have always been dubious, but the perception of “reliability” has held up, allowing for the rapid growth of LNG in recent years. That image is now shattered.

We have already seen how this kind of demand destruction play out. After Russia invaded Ukraine in early 2022, energy traders abruptly cancelled LNG contracts with countries like Bangladesh, Pakistan, and Sri Lanka and redirected tankers to the U.K. and Italy.

Energy traders made a killing. According Bloomberg, a shipment destined for Pakistan, at that time would have been worth $200 million in sales. Traders sold it in Europe for more than $600 million.

In the wake of the diversions, Pakistan and Bangladesh faced rolling blackouts. The resulting economic crisis in Pakistan nearly drove it to default. In response, the countries spent years negotiating long-term contracts with Gulf suppliers, only to see those contracts go up in smoke. In January, Bangladesh received the first shipment of a 15-year contract with QatarEnergy. Seven weeks later, QatarEnergy declared force majeure at its Ras Laffan facility. Facing a severe shortage, Bangladesh has now closed universities and instituted price rationing to save energy.

Pakistan is taking similar emergency measures, but unlike Bangladesh, Pakistan is in the midst of multi-year solar-driven energy revolution. Most of this growth has been off-grid or behind-the-meter. The Institute for Energy Economics and Financial Analysis (IEEFA) has calculated that over 25 years, Pakistan will save $3 billion in LNG costs for every gigawatt of solar it installs.

According to the World Economic Forum:

In 2024, Pakistan imported 17 gigawatts (GW) of solar photovoltaic (PV). The country also imported an estimated 1.25 gigawatt-hours (GWh) of lithium-ion battery packs in 2024. These are substantial additions to an energy system with approximately 40 GW of total installed capacity. If this trend continues, total battery imports could reach 8.75 GWh by 2030. This would be enough to meet over a quarter of peak demand, while solar could cover most daytime electricity needs.

Bangladesh, which has invested less in domestic renewables, “has considerably less cushion” according to the Diplomat.

Since 2024, Pakistan has actually struggled to absorb an LNG glut that threatened its gas infrastructure. Before the war, it was refusing delivery and renegotiating LNG contracts with Qatar and international gas companies like Eni as gas demand has fallen.

Energy Security = Energy Transition

The think tank Ember estimates that in 2025, the world added a record-breaking 814 GW of solar and wind capacity to its electrical grids. The current crisis will only accelerate this shift.

None of this is to say that transitioning to clean energy will be seamless. High energy prices are inflationary, which often causes interest rates to rise, making long-term capital expenditures—like solar and wind farms—harder to finance. High energy costs could also make some important climate initiatives less politically palatable. As Catherine Rampell of the Bulwark recently reported, Europe’s emissions trading system (ETS) and recent landmark Carbon Border Adjustment Mechanism (CBAM) — which had begun spurring other countries to introduce or expand their own carbon pricing systems — is facing serious pressure as European consumers push back on anything that raises prices. For the moment, though, the ETS appears to be holding, at least until it’s up for review again in July.

Then there’s the problem of materials. An article from Heatmap points out that oil isn’t the only thing affected by the war. Metal production is also disrupted. Aluminum producers in the region have already started shutting down production. Aluminum is used to make frames, mounts and racks in solar systems.

But while the rising cost of materials are a concern, by far the biggest variables in the installation cost of solar are “soft costs” — things like permits, labor, marketing — which is why, even though they have access to similarly-priced solar panels, per kilowatt, installed solar in Australia is a third of what it is the United States. Policy choices like net metering that make solar more or less economically valuable to end users are almost as important.

The oil shock of 2026 is different from those of the past. Renewables and the electrification of homes and transportation are more viable than ever. Solar and storage are orders of magnitude less expensive than they were in the 1970s and early 2000s. Electric vehicles are widespread, widely used, and getting more popular every year.

The energy security premium is real, and the energy transition is here. Absent a sudden reversion to a stable international order and the ability to cheaply produce vast new quantities of oil, the clean energy transition will only continue to accelerate.

Thanks for reading. I’d love to hear what you think — drop me a line, or connect with me LinkedIn.

To get these updates in your inbox, sign up here.